Institutional Insights: Goldman Sachs 'March FOMC Traders Take'

GS Views: March FOMC – Key Takeaways

GS US Economics Research Team Insights

- Impact of Iran War: Rising oil prices have led to revised forecasts for December 2026. Headline PCE inflation is up by 0.8pp to 2.9%, core PCE by 0.2pp to 2.4%, GDP growth lowered by 0.3pp to 2.2%, and peak unemployment rate increased by 0.1pp to 4.6%. Rate cuts are now expected in September and December 2026.

- March FOMC Meeting: The FOMC is likely to maintain the funds rate at 3.5-3.75%. The statement may highlight increased uncertainty due to the war, with potential inflationary pressures and subdued economic activity. Three dissents for a 25bp rate cut are anticipated. Projections for 2026 may show higher inflation (core: +0.2pp to 2.7%; headline: +0.6pp to 3.0%), lower GDP growth (-0.2pp to 2.1%), and a marginally higher unemployment rate (+0.2pp to 4.6%). Policy rate "dots" are expected to remain largely unchanged, indicating one cut each in 2026 and 2027.

- Warsh’s Stance: Warsh’s dovish outlook aligns with expectations of declining inflation. His views on reducing the Fed’s balance sheet significantly may face resistance, as the ample reserves framework is broadly supported. Shrinking the balance sheet without adjusting debt issuance could lower short-term rates but raise long-term rates, a politically and publicly contentious move.

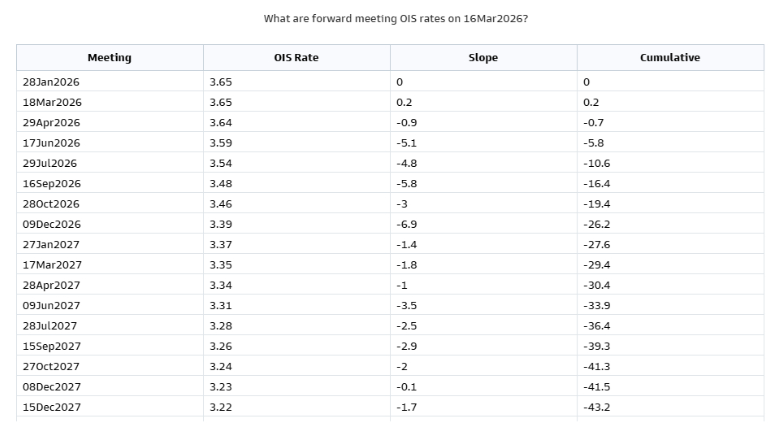

Rates:

- Last week, inflationary shocks in EUR & GBP spilled into USD, with SFRZ6 cheapening >50bps and terminal pricing hitting a cycle low of 20bps through Dec FOMC. Aggressive richening of put skew created pain for consensus short left-tail trades. Selling hikes in SFRM6 remains the most viable strategy, as a June hike under Warsh’s leadership is unlikely barring extraordinary circumstances.

- Macro volatility surged due to AI labor market fears and inflation risks from rising energy prices amid Iran conflict. Our franchise prefers receivers in 1y1y and 2y1y forwards but notes richened payers across forwards. Market awaits FOMC clarity on easing prospects or inflation caution amidst stress conditions.

FX:

- Geopolitics drives markets, oscillating between inflation impacts and recession risks. Fed rate cuts are now expected in September and December, reflecting inflation-growth tensions. Emphasis on inflation could support USD, AUD, CAD, and BRL, while recession risks may favor JPY despite negative terms of trade implications.

- Desk anticipates dovish tilt at FOMC, focusing on growth over inflation. EUR volatility is favored via delta-hedged puts, while USD positions are maintained with reduced deltas due to fast-paced US front-end repricing risks.

Equities:

- Fed likely to hold rates steady, citing war and oil price uncertainty. Growth concerns from oil prices or labor market weakness may drive easing expectations. Risks lean toward lower yields, favoring limited-risk exposure. Elevated equity vol persists, with SPX straddle pricing ~85bps. NDX options preferred over SPX due to skew. Hawkish dot plot could spook markets amidst Iran uncertainty.

Credit:

- Credit spreads widened due to macro weakness, stagflation fears, hyperscalers’ debt issuance, and private credit concerns. Volatility remains high, with CDX HY underperforming IG amid growth deterioration. ETF sell-offs (LQD, HYG) reflect stretched borrow and downside rate correlations. Credit risk premium may rise further amid worsening growth-inflation tradeoffs.

Commodities:

- Precious metals and copper remain correlated with macro assets, impacted by Middle East conflict. Gold faced liquidations under risk-off moves but retains favorable tail scenarios. Aluminum demand rose due to supply disruptions, though stockpiling may be limited. Metals positioning appears healthier, with Eastern demand supporting gold recovery if geopolitical tensions ease.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!