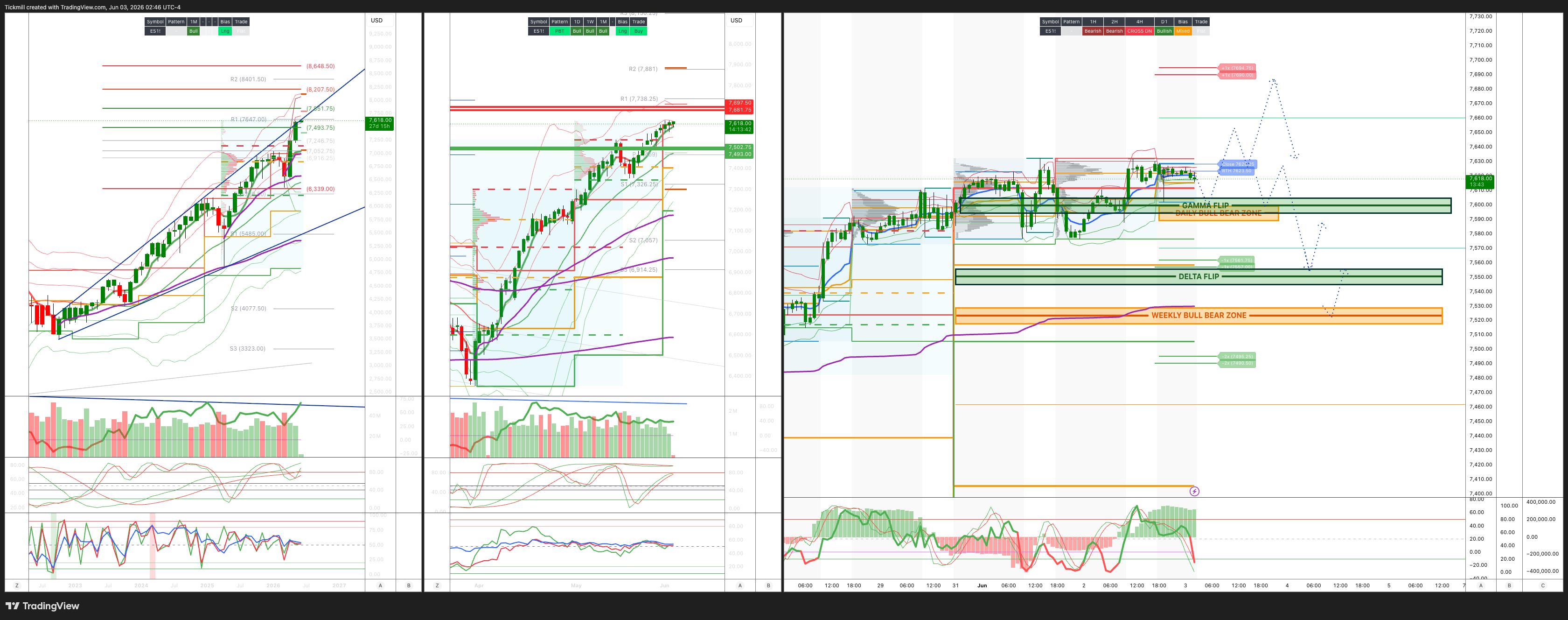

S&P500 Daily Action Areas & Price Targets 3/6/26

S&P500 Daily Action Areas & Price Targets 3/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

WEEKLY BULL BEAR ZONE 7535/25

WEEKLY RANGE RES 7680 SUP 7500

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.17 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7605

WEEKLY VWAP BULLISH 7480

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - OTFH 7595

WEEKLY STRUCTURE – OTFH - 7515

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7585/95

GAMMA FLIP 7600

DELTA FLIP 7550

DAILY RANGE RES 7690 SUP 7561

2 SIGMA RES 7756 SUP 7495

VIX BULL BEAR ZONE 19

TRADES & TARGETS

LONG ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET DAILY RANGE RES

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Mo’ Higher’

US equities extended higher, with the S&P 500 up 13bps to 7,610 on a $400m MOC buy imbalance, the Nasdaq 100 up 48bps to 30,661, the Russell 2000 up 90bps to 2,932, and the Dow up 45bps to 51,308. Volumes remained elevated at 20.58bn shares across US exchanges versus a YTD daily average of 19.1bn, reinforcing that the tape remains active beneath the surface even when the index move looks modest. Cross-asset moves were relatively contained outside of crypto and energy. VIX fell 174bps to 15.77, WTI rose another 157bps to $93.61, the 10-year yield was unchanged at 4.45%, gold was little changed at 4,490, DXY was flat at 99.19, and Bitcoin fell sharply, down 590bps to 67,145.

The headline story was a violent rebound in Momentum. Goldman’s high momentum basket, GSPRHIMO, rose 7%, its biggest one-day move higher ever, driven by both longs moving higher and shorts moving lower. This is an important shift after the prior two sessions were dominated by the historic software squeeze and underweight catch-up. Today’s action looked more like a reassertion of AI/semi/hardware leadership, with momentum factor strength returning sharply and software giving back some of its recent outperformance. The market remains risk-on, but the leadership baton is rotating extremely quickly.

The catalyst for the momentum move appears to have been follow-through strength from overnight and pre-market AI infrastructure headlines. MRVL rose 32% after Nvidia’s Jensen Huang reportedly called it the next $1tn company. HPE rose 20% after a strong earnings print and raised guide. AVGO rose 5%, while peripheral AI and semiconductor plays rallied in sympathy. A large capital raise this week also appears to have driven another leg higher in Semis and AI infrastructure, reinforcing the idea that the market is still willing to reward companies tied to compute, networking, ASICs, memory, and AI data-center buildout.

At the same time, the move created a reversal in recent software strength. After software’s historic two-day outperformance versus the S&P 500, investors were forced to revisit the disintermediation debate. The question is whether the latest AI capital raise and renewed hardware/infrastructure momentum accelerate concerns that parts of application software and traditional SaaS are vulnerable to AI-native competition or margin pressure. That does not mean all software is impaired; security, data infrastructure, and AI-enabling platforms remain better positioned. But the blanket SaaS squeeze paused as investors rotated back into hardware, semis, and high-momentum AI beneficiaries.

Financials had a difficult session, especially exchanges. CBOE, CME, and NDAQ were all down more than 3% as the market digested potential business-model impacts and overhang from perpetual futures. The concern is that broader adoption or regulatory progress around perpetual futures could affect trading volumes, fee pools, market structure economics, and competitive positioning for incumbent exchange operators. This is a classic example of how AI and market-structure disruption themes are no longer confined to Tech; they are now creating sharp dispersion across Financials as well.

Health Care was also heavy and appeared impacted by source-of-funds dynamics. In a market where investors are chasing AI infrastructure, semis, momentum, and select high-beta themes, defensives and lower-momentum areas can become funding sources. Health Care has not been the epicenter of negative fundamental news, but it remains vulnerable when portfolio managers need to raise capital for higher-conviction, higher-velocity trades elsewhere. That fits the broader tape: factor and thematic pressure are dominating sector fundamentals on many days.

Floor activity was moderate at 5 out of 10, but the desk finished meaningfully skewed to buy at +377bps versus a 30-day average of +81bps. Asset managers were slight net buyers, driven by demand across Tech, Industrials, and Health Care, offset by supply in Utilities and REITs. Hedge funds also finished slight net buyers, with broad demand across sectors excluding TMT. The “ex-TMT” detail matters because even though Tech led on the screen, hedge funds were not necessarily the marginal buyer of TMT on the day. This supports the idea that some of the AI/semi move was being driven by fast money, options, retail, systematic flows, or index/thematic demand rather than straightforward long/short stock picking.

After the bell, PANW rose 9% after reporting above the high end of its guided range for fiscal 3Q. The stock is now up more than 100% in a month, which captures the intensity of the security/software re-rating. Cybersecurity continues to stand out as a better-quality area within software because investors can more easily connect AI, cloud complexity, identity, and threat-surface growth to durable demand. PANW’s strength may help stabilize the software narrative after the intraday profit-taking, but the group is now moving so quickly that strong prints can be rewarded while still creating valuation and crowding concerns.

Derivatives activity was slower, with S&P spot and volatility closing little changed. The main index-vol story was the outperformance of Russell 2000 and Nasdaq vol alongside their stronger spot moves. Skew steepened across the board despite all major indices closing green, meaning downside protection became relatively more expensive even as equities advanced. That is notable because earlier in the rally, put-call skew had compressed to extreme lows. A steepening skew on an up day suggests some investors are beginning to add protection into strength, or at least that upside chasing is no longer the only volatility flow.

Flow-wise, the desk saw buyers of forward volatility in S&P and sellers of short-dated forward volatility in Russell. The desk continues to think selling Russell 2000 one-month to three-month forward volatility screens attractively, with levels in the 85th percentile on a one-year lookback ahead of the Russell rebalance. The logic is that the rebalance may graduate larger and more volatile names out of the index, potentially reducing future realized volatility. With small caps finally outperforming on the day but still lagging the broader AI/Tech-led tape, the vol surface may be pricing more event risk than the desk expects to realize.

In thematic and single-name volatility, the Goldman TMT Momentum Pair rose 9.5%, its second-largest one-day move in the past five years, just behind the 9.63% move on April 8. This confirms that the day was dominated by factor violence rather than simple index direction. The desk saw profit-taking in software names that had rallied into today and in quantum names, with the GS quantum basket up another 2%. The key point is that investors are not de-risking broadly; they are rotating aggressively between AI subthemes. Software squeeze winners are being trimmed, hardware/semis are being chased, and speculative AI-adjacent areas like quantum remain active.

The S&P implied move through the end of the week is now 86bps. With the S&P closing at 7,610, that implies roughly 65 points of movement and an approximate range of 7,545 to 7,675. The market remains close to the upper end of recent implied ranges, and the macro calendar still includes ISM Services and payrolls. A benign macro backdrop would likely allow the rotation to continue, with AI infrastructure, semis, cybersecurity, and select high-momentum names staying bid. A hot data print that pushes yields higher could complicate the move, especially for long-duration growth and the most extended momentum pockets. A weak growth print could shift the debate back toward defensives, Health Care, and quality, though recent source-of-funds dynamics suggest those groups need more than just valuation support to lead.

The market continues to grind higher, but the internals remain exceptionally unstable. Monday was about software’s historic squeeze; Tuesday was about the largest-ever one-day move in a high-momentum basket and a renewed AI infrastructure/semi bid. The S&P’s 13bp gain hides extreme factor churn, with momentum, software, financial exchanges, Health Care, quantum, and small-cap volatility all moving sharply beneath the surface. The rally is still supported by flows, buybacks, retail, CTAs, and hedge fund net exposure, but leadership is rotating faster than fundamental narratives can adjust. That argues for respecting the upside trend while staying selective: prefer AI infrastructure, semis, security, and data infrastructure over broad SaaS beta, watch exchange disruption risk in Financials, and use strength to add protection where skew is no longer as historically cheap as it was last week.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!