Daily Market Outlook, May 21, 2024

Daily Market Outlook, May 21, 2024

Munnelly’s Macro Minute…

“Asian Markets Snap A Seven Day Winning Streak”

Asian stocks paused on Tuesday after a seven-day winning streak. Profit-taking by investors led to a decline in Chinese stocks. Hong Kong's equity market also experienced a downturn, with Li Auto leading the losses in the MSCI Asia Pacific index due to lower-than-expected first-quarter vehicle sales. Japanese stocks remained steady thanks to positive insurance company earnings. The economic challenges in China remain a major concern in Asia, with recent data showing no signs of recovery in the country's debt-ridden real estate market. Land sales last month generated the lowest revenue for local governments in eight years, highlighting the financial struggles faced by agencies heavily reliant on this type of income.

This week's main data releases are set for later in the week, leaving today's schedule relatively light. In the UK, the May CBI industrial trend survey will offer an update on the factory sector. The April survey revealed that orders remained very weak, while selling price inflation reached its highest level since February 2023. It will be interesting to see if the May data indicates any improvement. The most anticipated data release of the week is the UK April CPI inflation report, due early tomorrow. According to consensus forecasts, the year-on-year headline rate is expected to drop sharply to 2.1% from 3.2% in March, marking the lowest rate since July 2021. This decrease is primarily due to an approximately 12% reduction in the Ofgem energy price cap. UK core CPI inflation, which excludes food and energy, is also expected to fall to 3.6% from 4.2%. However, this rate remains higher than the headline rate, with services inflation predicted to stay above 5%. While the anticipated drop in inflation is positive news, it remains uncertain whether Bank of England policymakers will see it as enough progress to justify an interest rate cut.

The Eurozone is anticipated to report a larger trade surplus in April compared to March, continuing the recent trend of increasing surpluses. This is mainly due to a decrease in import costs following a drop in gas prices earlier in the year. However, the recent rise in gas prices in May could potentially disrupt this trend.

Today, several central bank policymakers, including European Central Bank President Lagarde and Bank of England Governor Bailey, are scheduled to speak. They are expected to speak at events where they are unlikely to address near-term monetary policy.

Stateside, there will be more Fedspeak as Governor Christopher Waller and four regional Fed bosses are scheduled to speak at different events. The minutes of the Fed's previous policy meeting, which are due on Wednesday, will be important, but they do not reflect the recent decrease in CPI after three consecutive months of higher-than-expected results.

Overnight Newswire Updates of Note

RBA Resumes Rate-Hike Discussion On Renewed Inflation Concerns

NZ Tsy: There Is No Near-Term Turning Point Seen For The Economy

Fed’s Mester: Fcst Of 3 Cuts This Year Is Now Probably Too Many

Fed’s Daly Says There's No "Urgency" To Adjust Interest Rates

Oil’s Market Metrics Point To Weak Outlook Ahead Of OPEC+ Meet

Russia Suspends Ban On Gasoline Exports Until June 30, Gov Says

Dell Deepens AI Push With New PCs, Nvidia-Powered Servers

GSK Faces Whistleblower Suit From Lab That Found Zantac Risk

Rio Tinto Invokes Force Majeure On Australian Alumina Sales

Samsung Elec. Picks Vet Exec To Tackle 'Chip Crisis' Amid AI Boom

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0800 (631M), 1.0840-50 (2.1BLN), 1.0860 (320M), 1.0900 (942M)

USD/CHF: 0.9055 (1.9BLN), 0.9100 (383M). EUR/CHF: 0.9850 (898M)

GBP/USD: 1.2600 (210M), 1.2625-30 (718M)

EUR/GBP: 0.8600 (433M), 0.8650 (200M)

AUD/USD: 0.6565-75 (1.6BLN), 0.6650 (226M), 0.6675 (200M), 0.6705-15 (511M)

AUD/NZD: 1.0850 (304M). EUR/AUD: 1.6300 (200M)

USD/CAD: 1.3600 (460M), 1.3640-45 (1.4BLN), 1.3700 (1.3BLN)

USD/JPY: 154.50 (795M), 156.75 (295M), 157.00 (400M), 157.75 (590M)

AUD/JPY: 102.75 (330M)

It is anticipated that the RBNZ will maintain rates at 5.5% on Wednesday, but there is still a possibility of NZD volatility. The market is pricing in a 44bps cut in 2024, whereas the previous RBNZ forecast indicated the first cut in Q1 2025. Overnight NZD/USD FX options now expire after the RBNZ meeting, so there may be a reaction in the FX market. Implied volatility reflects higher expectations for realized volatility, with overnight rates at 10 to 15.0 and premium/break-even at 25 to 38 USD pips in either direction. Additionally, other short-dated NZD options are influenced by related event risk premiums.

CFTC Data As Of 17/05/24

Japanese yen net short position is -126,182

British pound net short position is -20,075

Euro net long position is 17,155 contracts

Swiss franc posts net short position of -41,107

Bitcoin net short position is -177 contracts

Equity fund managers raise S&P 500 CME net long position by 60,168 contracts to 920,863

Equity fund speculators increase S&P 500 CME net short position by 40,882 contracts to 279,337

Gold NC Net Positions: $204.5K vs $199.6K

Technical & Trade Views

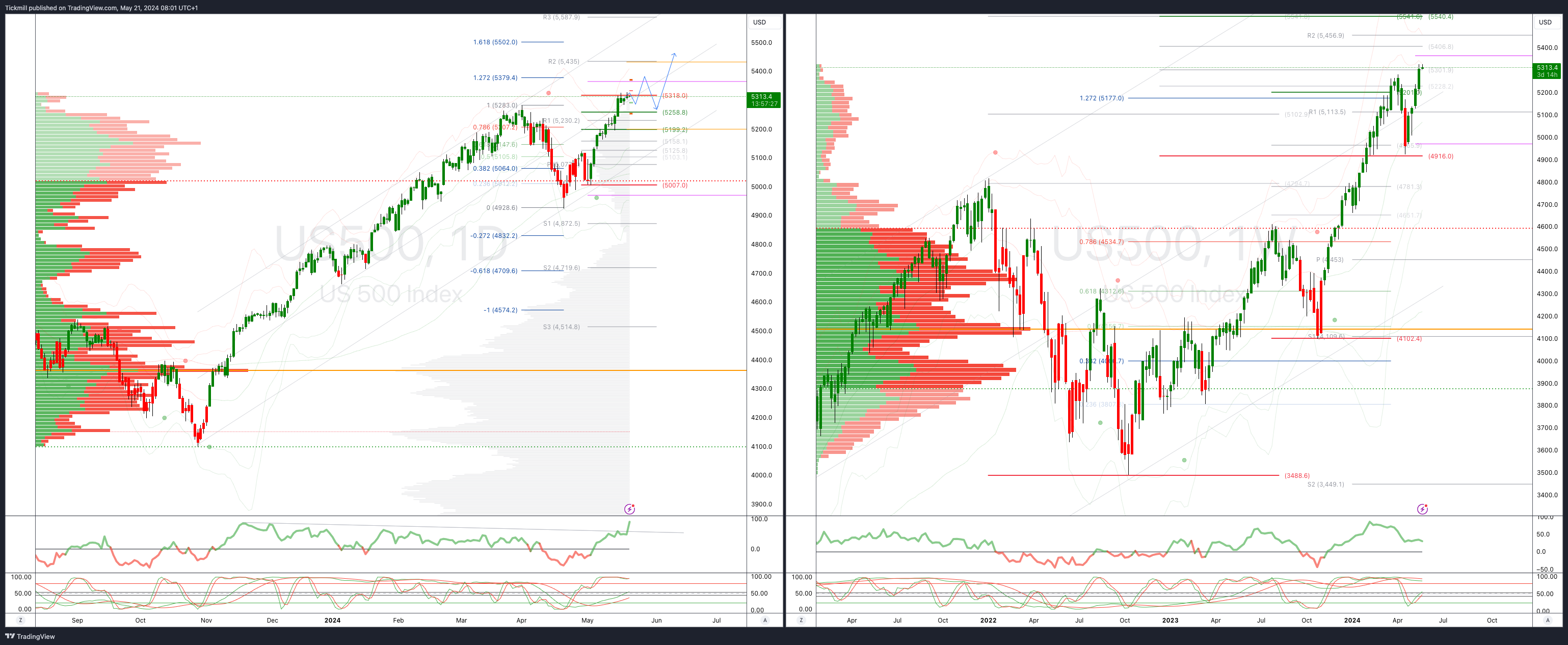

SP500 Bullish Above Bearish Below 5280

Daily VWAP bullish

Weekly VWAP bullish

Below 5258 opens 5200

Primary support 5160

Primary objective is 5379

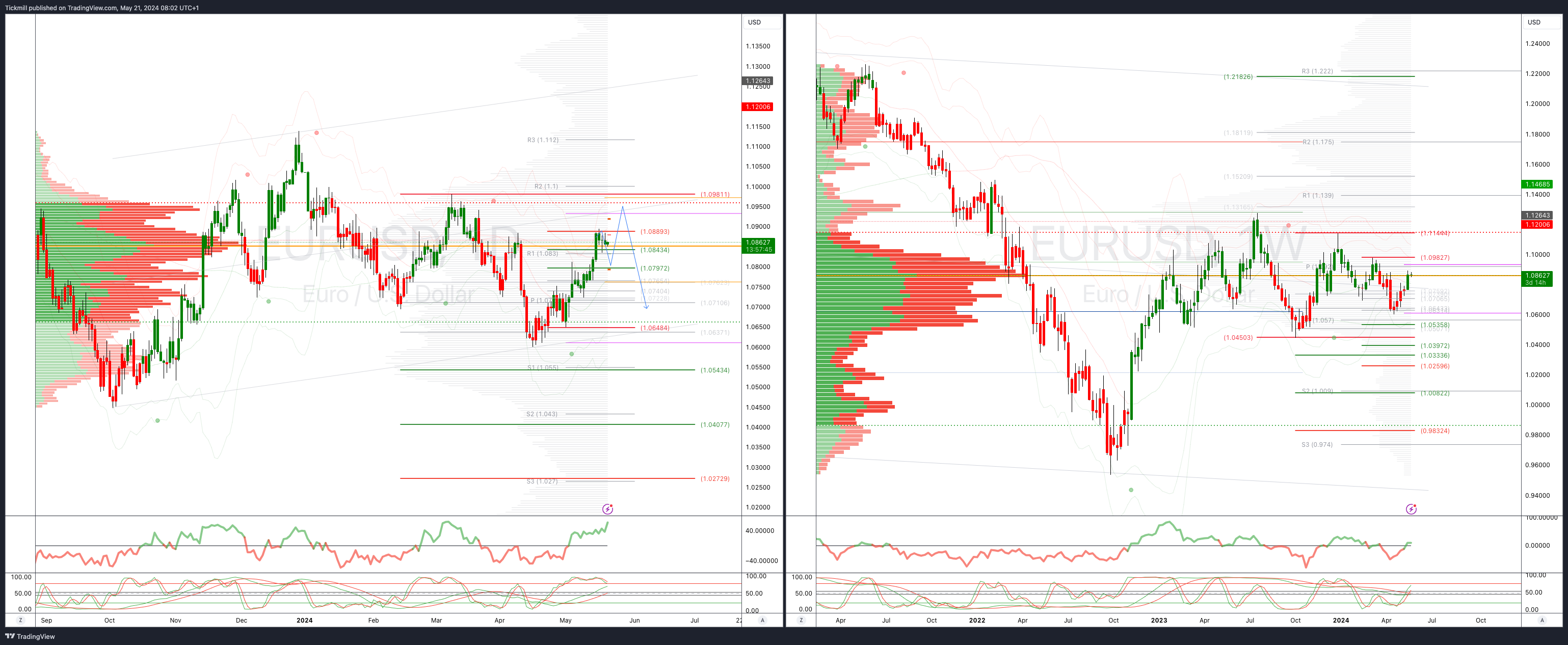

EURUSD Bullish Above Bearish Below 1.08

Daily VWAP bullish

Weekly VWAP bullish

Above 1.10 opens 1.11

Primary resistance 1.0981

Primary objective is 1.0550

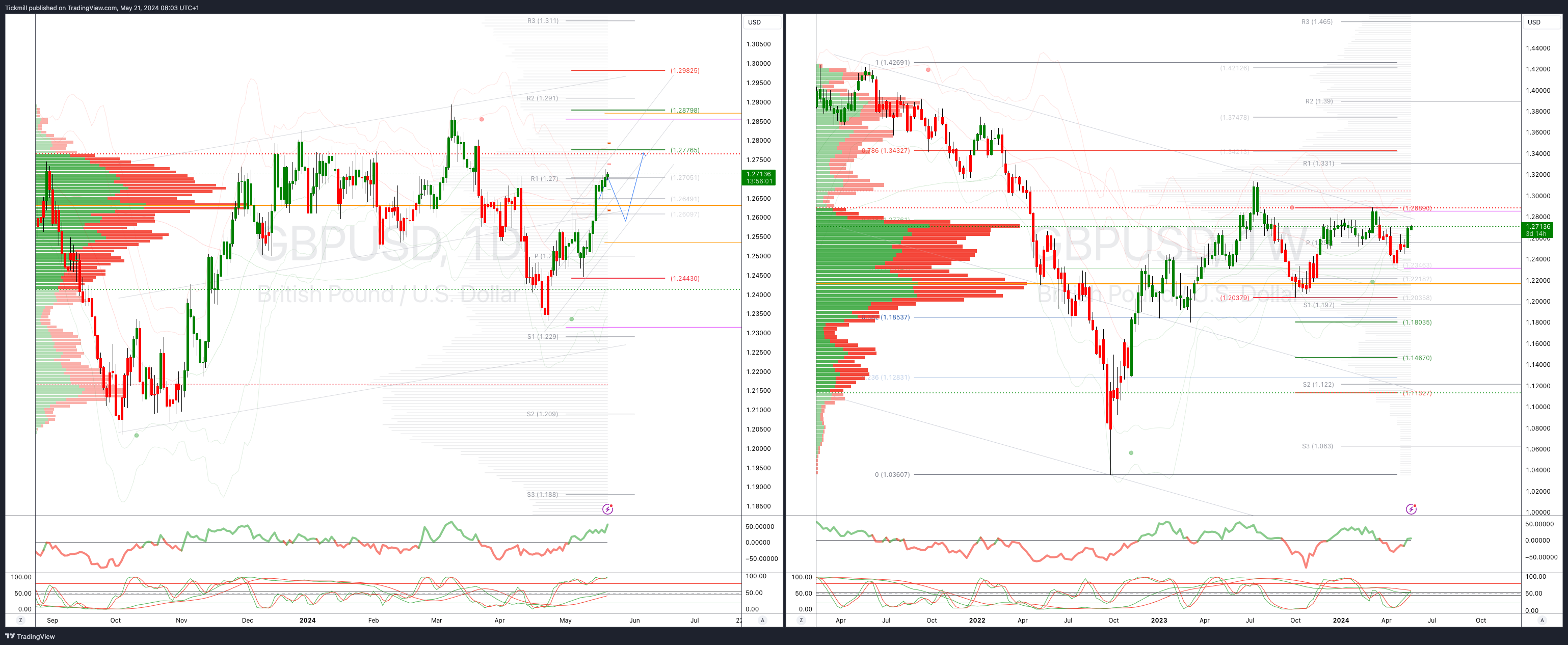

GBPUSD Bullish Above Bearish Below 1.2630

Daily VWAP bullish

Weekly VWAP bullish

Below 1.2600 opens 1.2540

Primary support is 1.2443

Primary objective 1.2776

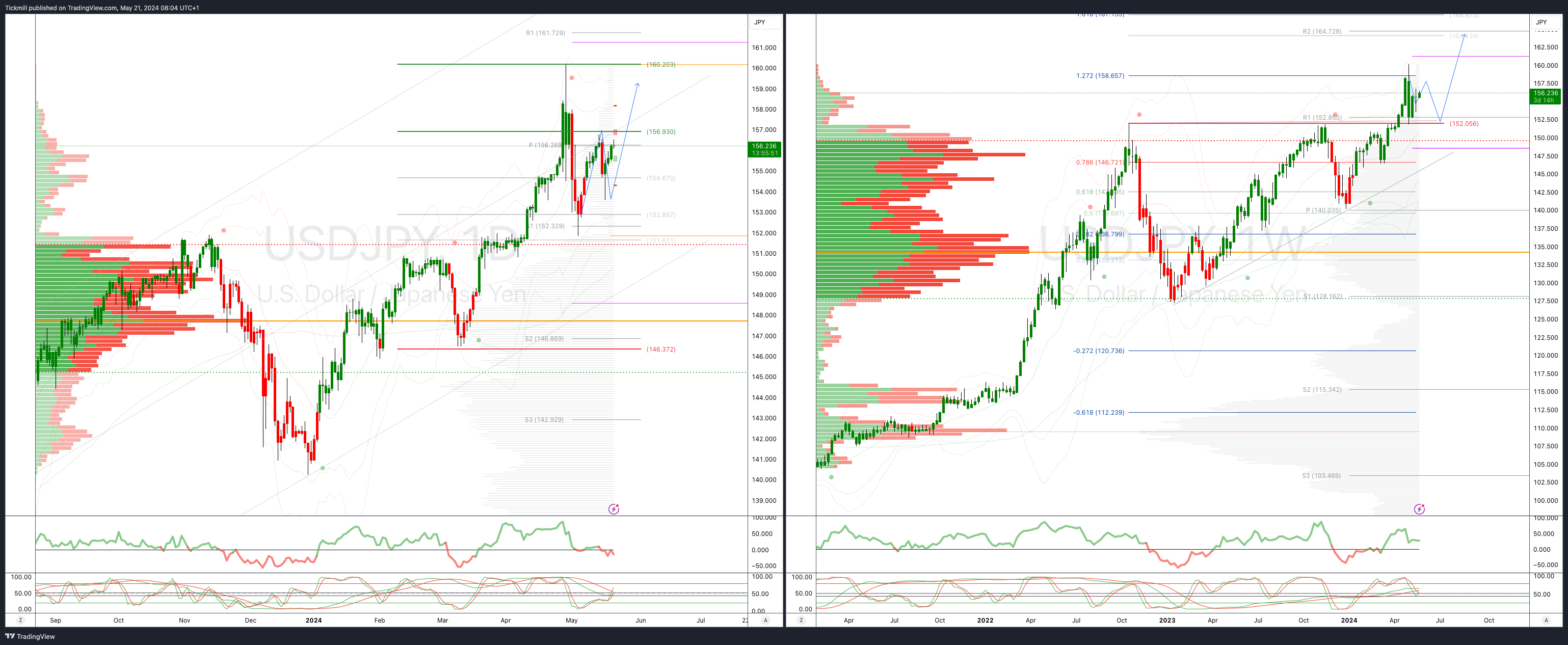

USDJPY Bullish Above Bearish Below 152

Daily VWAP bullish

Weekly VWAP bullish

Below 154.40 opens 152

Primary support 152

Primary objective is 165

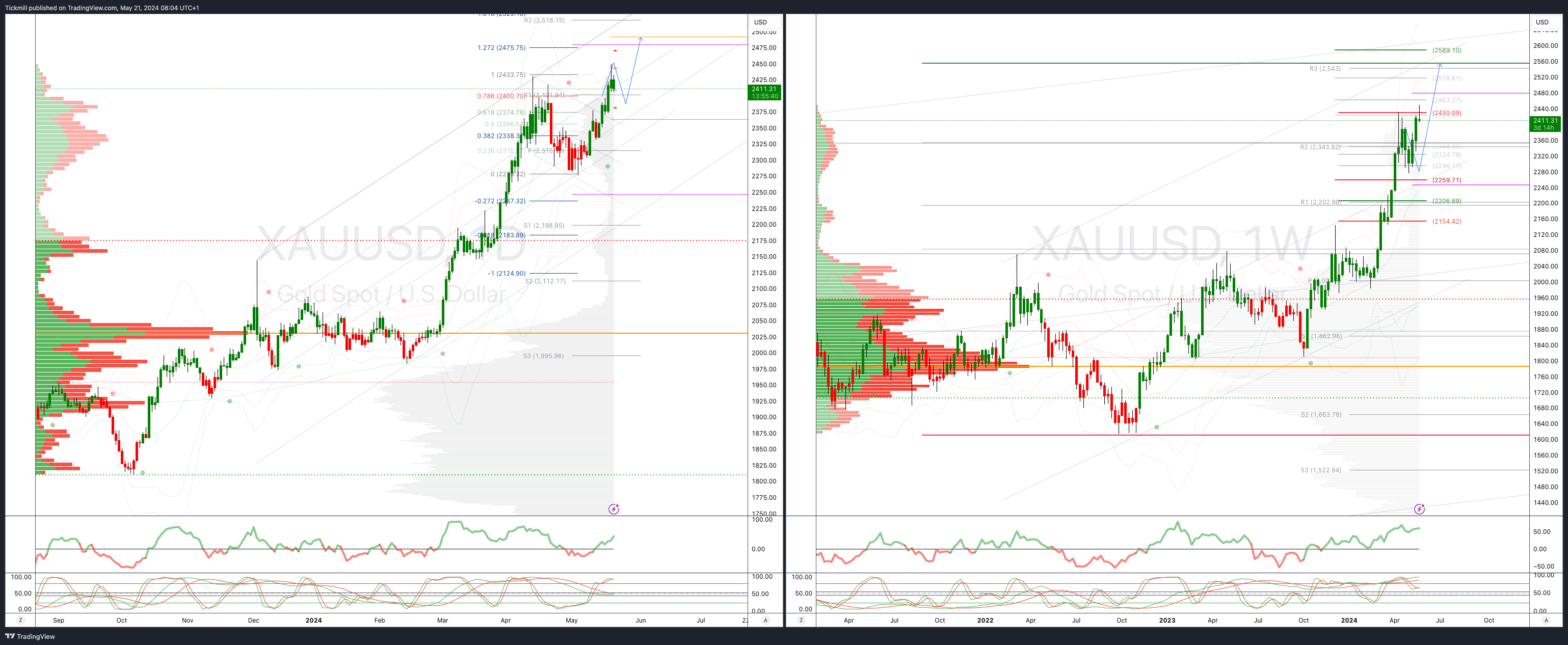

XAUUSD Bullish Above Bearish Below 2376

Daily VWAP bullish

Weekly VWAP bullish

Below 2330 opens 2240

Primary support 2260

Primary objective is 2560

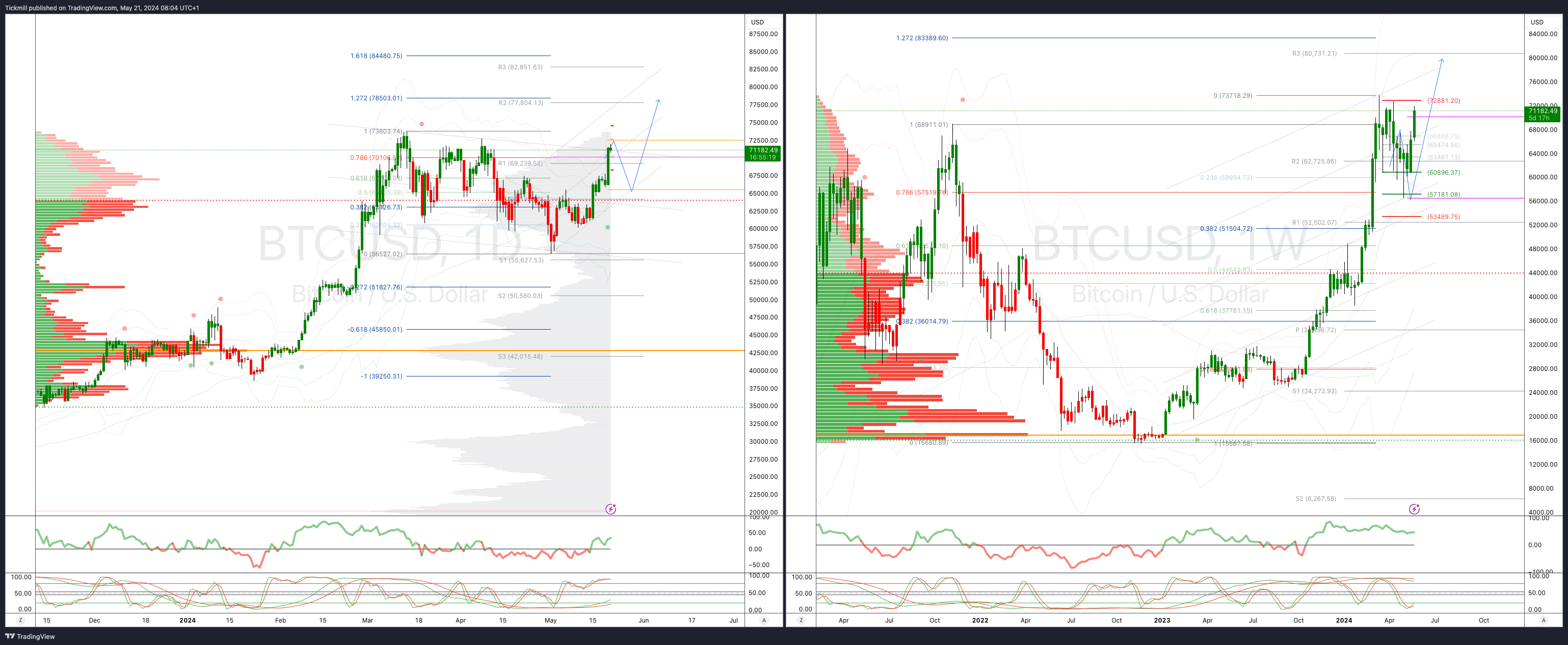

BTCUSD Bullish Above Bearish below 65500

Daily VWAP bullish

Weekly VWAP bullish

Above 70500 opens 78500

Primary support is 65000

Primary objective is 78500

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!