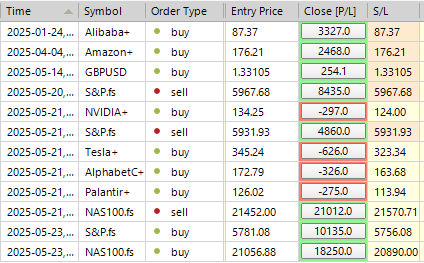

SP500 LDN TRADING UPDATE 27/05/25

SP500 LDN TRADING UPDATE 27/05/25

WEEKLY BULL BEAR ZONE 5840/50

WEEKLY RANGE RES 5945 SUP 5849

DAILY VWAP BULLISH 5868

WEEKLY VWAP BULLISH 5797

DAILY ONE TF DOWN 5843

WEEKLY BALANCE 5987-5780

MONTHLY BALANCE

GAP LEVELS 5741/5710

WEEKLY ACTION AREA VIDEO TO FOLLOW AHEAD OF NY OPEN

GOLDMAN SACHS TRADING DESK VIEWS

U.S. EQUITIES UPDATE: WEEKLY RECAP

FICC and Equities | 23 May 2025 | 8:16 PM UTC

Market Performance:

- S&P 500: -67bps, closing at 5,802, with a MOC buy imbalance of $1B.

- Nasdaq 100 (NDX): -93bps, ending at 20,915.

- Russell 2000 (R2K): -51bps, finishing at 2,040.

- Dow Jones: -61bps, closing at 41,603.

- Trading Volume: 17.9 billion shares traded across all U.S. equity exchanges, above the YTD daily average of 16.5 billion.

- Volatility Index (VIX): +10%, closing at 22.39.

- Other Markets: Crude oil +62bps to $61.57, U.S. 10-Year Treasury yield -1bp at 4.51%, gold +200bps to $3,390, DXY -86bps at 99.10, Bitcoin -228bps to $108,558.

Market Context:

U.S. stocks declined heading into the long weekend, with the S&P 500 down 261bps for the week. Headlines focused on President Trump’s proposal of a 50% tariff on the European Union if trade negotiations fail by June 1st. Additional pressure came from a Moody’s downgrade, weak Japanese bond auction results, higher UK CPI, and ongoing deficit concerns.

Desk Flows:

- Long-Only Funds (LOs): Net sellers of $2B this week.

- Hedge Funds (HFs): Flat overall, with activity concentrated in macro products as higher yields dampened risk appetite.

- Sector Trends: Mega-cap tech outperformed non-profitable tech, with the pair up ~5% for the week. Google (GOOGL) was a standout performer amid improving tactical sentiment.

Prime Brokerage (PB):

- U.S. equities saw modest net buying, with gross trading activity increasing. Long buys outpaced short sales at a ratio of 1.3:1.

- Hedge funds bought Health Care stocks for the fourth consecutive week, with long buys outpacing shorts at a 4.3:1 ratio.

- Consumer Discretionary and Consumer Staples were the most net-sold sectors. Discretionary saw its fastest net selling pace in five weeks and remains the most net-sold sector YTD, while Staples experienced the largest net selling in seven weeks.

Derivatives Activity:

- Markets sold off aggressively following President Trump’s tariff comments targeting Apple and the European Union.

- Clients monetized downside exposure and added VIX upside through call spreads as markets rebounded intraday.

- Volatility and short-dated skew remained firmly bid throughout the session.

- The desk views VIX upside out to July as a strong hedge ahead of the tariff deadline. NDX call spreads also appear favorable as a delta replacement ahead of Nvidia (NVDA) earnings.

Looking Ahead:

- S&P 500 Implied Move: 2.07%.

- Market Schedule: U.S. markets will close Monday for Memorial Day.

- Key Events: Focus on Fed commentary, NVDA earnings (Wednesday), and macro data releases including FOMC Minutes (Wednesday), GDP second reading (Thursday), and PCE & University of Michigan Sentiment (Friday).

- Tax Bill Negotiations: Watch for updates as the bill moves to the Senate following House approval this week.

- NVDA Outlook: Desk positions NVDA as a 7.5/10. The stock is ~50% above its April low but has been range-bound over the past year amidst normalizing revenue beats and mixed geopolitical and AI-related headlines.

Kostin’s Kickstart:

- Mutual funds and hedge funds have delivered positive returns YTD despite market turbulence.

- U.S. long/short hedge funds are up +2% YTD, according to GS PB estimates.

- Top “shared favorites” this quarter: APP, BAC, CRH, MA, SCHW, SPOT, and V. New additions include BAC and SCHW.

- The overlap of mutual fund and hedge fund favorites has returned 9% YTD, outperforming the S&P 500’s flat performance.

- The “Magnificent 7” (excluding TSLA) remain key constituents of Hedge Fund VIPs but are underweighted by mutual funds.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!