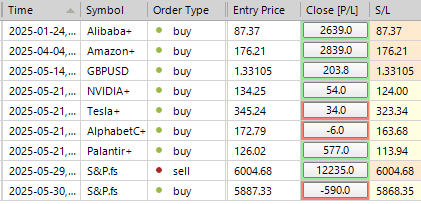

SP500 LDN TRADING UPDATE 02/06/25

SP500 LDN TRADING UPDATE 02/06/25

WEEKLY BULL BEAR ZONE 5795/5805

WEEKLY RANGE RES 6020 SUP 5805

DAILY VWAP BULLISH 5897

WEEKLY VWAP BULLISH 5816

DAILY BALANCE 4 DAY 5956/5853

WEEKLY BALANCE 2 WEEK 5987/5780

MONTHLY BALANCE 3 MONTH 5997/4876

GAP LEVELS 5843/5741/5710

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favoring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Up (OTFU): This represents a market trend where each successive bar forms a higher low, signaling a strong and consistent upward movement.

One-Time Framing Down (OTFD): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement..

WEEKLY ACTION AREA VIDEO TO FOLLOW AHEAD OF NY OPEN

GOLDMAN SACHS TRADING DESK VIEWS

U.S. EQUITIES UPDATE: Weekly Insights

FICC and Equities | 30 May 2025 |

Market Performance:

The S&P 500 closed the shortened trading week up +188bps, marking a +6.15% gain for May—the strongest May performance since 1997.

Flows Overview:

- Asset Managers: Ended the week as net sellers (-$4B), leveraging the MSCI rebalancing as a liquidity event. Selling activity was concentrated in technology and consumer sectors.

- Hedge Funds (HFs): Closed as slight net buyers (+$800M), with strong demand in tech (boosted by better-than-expected NVDA guidance), consumer (momentum in BIRK and AS FOs), and macro-related products.

- Supply: Paper issuance totaled $7B this week (vs. YTD weekly average of $3B). Hedge fund demand remains robust, though signs of investor fatigue and uncertainty ("what's next") linger, particularly around tariffs.

Next Week’s Focus:

The S&P 500 implied move through June 6 is 1.94%, with a balanced mix of macro and micro events. Key scheduled highlights include:

- Economic Data:

- US Manufacturing ISM (Mon)

- Eurozone CPI & US JOLTs (Tues)

- US Services ISM & Beige Book (Wed)

- US Payrolls (Fri)

- Central Bank Meetings:

- Bank of Canada (Wed)

- ECB (Thurs)

- RBI (Fri)

- Earnings Reports:

- Consumer: CPB, DG, DLTR, FIVE, PVH, LULU, MTN, VSCO

- Tech: CRWD, HPE, MDB, CIEN, AVGO, DOCU

Prime Brokerage Trends:

US equities were net bought for the fourth consecutive week, primarily driven by long positions.

- Long Buying: This week’s single-stock long buying was the largest since November (97th percentile over 5 years), signaling heightened hedge fund appetite for idiosyncratic risk.

- Sector Trends: 10 of 11 US sectors were net bought, with Information Technology leading the charge, recording the largest dollar-based long buying in over a decade.

- Leverage Metrics:

- US Fundamental L/S Gross Leverage rose +0.5 pts to 213.1% (99th percentile over 3 years).

- US Fundamental L/S Net Leverage climbed +2.1 pts to 50.3% (30th percentile over 3 years), marking the largest increase in 7 weeks.

Derivatives Insights:

A volatile trading session saw markets sell off following another Friday Trump tweet but recover to close flat. Volatility remained stable overall.

- Flows: Clients monetized downside positions during the sell-off, while flows were quieter during the recovery—indicative of added length by clients.

- Gamma Dynamics: Dealers stayed light on gamma, maintaining a streak of being long less than $2B of S&P gamma for 67 consecutive days—approaching a 5-year record.

- Next Week Outlook: Macro data will take center stage with ISM, ADP, and NFP reports due. The straddle for next week closed at ~1.75%.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!