S&P500 Daily Action Areas & Price Targets 4/6/26

S&P500 Daily Action Areas & Price Targets 4/6/26

***QUOTING ES1! FOR CASH US500 EQUIVALENT LEVELS, SUBTRACT POINT DIFFERENCE***

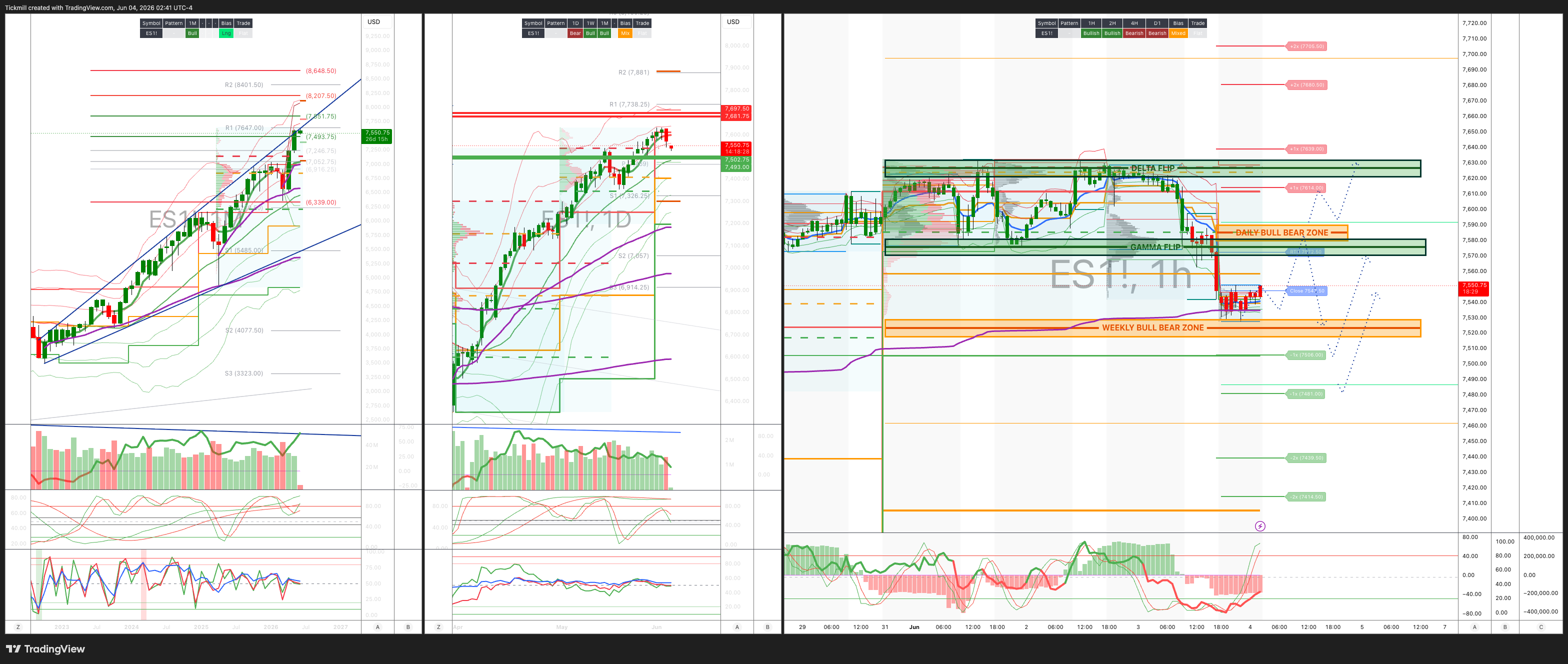

WEEKLY BULL BEAR ZONE 7535/25

WEEKLY RANGE RES 7680 SUP 7500

June MOPEX Straddle: 274pt range implies a OPEX to OPEX range of [7134, 7683]

June QOPEX Straddle is 546.4pt giving us a range of [5960,7052]

JHEQX Q2 Collar 6189/6290 - 6865/6955

DEC2025 OPEX to DEC2026 OPEX is 945 points giving us a range of [5889,7779]

SPX PUT/CALL RATIO 1.17 (The numbers reflect options traded during the current session. A put-call ratio below 0.7 is generally considered bullish, and a put-call ratio above 1.0 is generally considered bearish)

DAILY VWAP BULLISH 7605

WEEKLY VWAP BULLISH 7480

MONTHLY VWAP BULLISH 7036

DAILY STRUCTURE - BALANCE 7562/7632

WEEKLY STRUCTURE – OTFH - 7515

MONTHLY STRUCTURE - OTFH - 7199

Balance: This refers to a market condition where prices move within a defined range, reflecting uncertainty as participants await further market-generated information. Our approach to balance includes favouring fade trades at the range extremes (highs/lows) while preparing for potential breakout scenarios if the balance shifts.

One-Time Framing Higher (OTFH): This represents a market trend where each successive bar forms a higher low, signalling a strong and consistent upward movement.

One-Time Framing Lower (OTFL): This describes a market trend where each successive bar forms a lower high, indicating a pronounced and steady downward movement.

DAILY BULL BEAR ZONE 7585/95

GAMMA FLIP 7600

DELTA FLIP 7550

DAILY RANGE RES 7639 SUP 7481

2 SIGMA RES 7680 SUP 7414

VIX BULL BEAR ZONE 19

TRADES & TARGETS

SHORT ON REJECT/RECLAIM DAILY BULL BEAR ZONE TARGET

LONG ON REJECT/RECLAIM DAILY RANGE SUP TARGET CLOSE>RTH

***ADDITIONAL SETUPS & TARGETS HIGHLIGHTED ON THE CHARTS***

(I FADE TESTS OF 2 SIGMA LEVELS ESPECIALLY INTO THE FINAL HOUR OF THE NY CASH SESSION AS 90% OF THE TIME WHEN TESTED THE MARKET WILL CLOSE ABOVE OR BELOW THESE LEVELS)

GOLDMAN SACHS TRADING DESK VIEW - ‘Breather’

US equities sold off as the market absorbed a more difficult combination of higher oil, higher rates, higher volatility, renewed Middle East risk, and fresh tariff headlines. The S&P 500 fell 74bps to 7,554 with a $935m MOC sell imbalance, the Nasdaq 100 declined 29bps to 30,571, the Russell 2000 dropped 131bps to 2,893, and the Dow fell 121bps to 50,687. Volumes remained above average at 19.77bn shares across US equity exchanges versus a YTD daily average of 19.1bn. Cross-asset moves were clearly risk-negative: VIX rose 203bps to 16.09, WTI crude jumped 271bps to $96.29, the US 10-year yield rose 5bps to 4.90%, gold fell 109bps to 4,440, DXY gained 31bps to 99.53, and Bitcoin dropped 327bps to 65,315.

The surprising part of the day was that the Nasdaq 100 was only down roughly 30-35bps despite the move in rates, vol, and oil. In a more conventional tape, a 5bp rise in the 10-year yield to 4.90%, a stronger dollar, and renewed geopolitical risk would have produced a larger drawdown in long-duration growth. Instead, single-stock question volume was very elevated, and the market conversation remained focused more on thematic and sector tilts than broad index de-risking. This is consistent with the recent pattern of factor volatility exceeding index volatility. Investors are not simply selling everything; they are rotating aggressively between AI infrastructure, software, megacap Tech, small caps, cyclicals, defensives, and source-of-funds sectors.

The overnight macro backdrop was materially less friendly. Reports that US forces intercepted Iranian missiles brought Middle East escalation risk back into focus, while the White House formally proposed new tariffs of at least 10% on imports from major trading partners, including the EU, Canada, and Mexico. China, Japan, Brazil, and several others would reportedly face a 12.5% rate. This combination matters because it challenges the two supports that had helped the market rally in May: geopolitical de-escalation and confidence that earnings upgrades could continue without a renewed inflation shock. Higher oil and new tariff proposals both push in the direction of higher input costs, potential margin pressure, and more complicated inflation dynamics.

TMT was very active around the open, though activity normalized as the session progressed. There were buyers in supercap Tech after the GOOG/GOOGL follow-on offering, which marked the largest US equity capital raise in history at $35bn, surpassing the previous record held by Boeing. The ability of the market to absorb a record-sized offering and still find buyers in supercap Tech is important. It speaks to the depth of demand for large-cap AI and platform exposure, even as concerns about issuance supply remain a broader market overhang. However, the offering also reinforces the theme that the market is being asked to absorb a very large amount of equity supply at a time when positioning in megacap Tech is already elevated.

The floor was moderate in terms of activity, at 5 out of 10, but the flow skew turned meaningfully negative. The desk finished 650bps for sale versus a 30-day average of +72bps. Both asset managers and hedge funds were better sellers, with broad supply across discretionary, macro products, utilities, and pockets of Tech. This is a notable change from the prior sessions, when the desk had finished materially skewed to buy. It suggests that the combination of oil, rates, tariffs, and geopolitical risk finally triggered some de-risking, even though index losses remained fairly contained.

The post-bell tape added to the sense that earnings bars are becoming increasingly difficult to clear. AVGO fell 8% after results, as the magnitude of the beat was not enough versus an elevated bar. This is important for the AI infrastructure complex because Broadcom has been one of the key beneficiaries of the renewed semiconductor and custom silicon trade. The stock’s reaction does not necessarily invalidate the AI thesis, but it shows that expectations are now extremely high. When a strong print is not enough, the market is telling investors that positioning and valuation are starting to matter again.

FIVE fell 7% after reporting what was broadly viewed as a big beat and a large raise, but the stock still traded lower because the result missed some of the very high bogeys circulating among investors. The 2Q guide in the high-single-digit range was expected by most, but expectations had clearly moved above what the company delivered. This creates an interesting debate because FIVE remains one of the better retail stories at the moment, yet the bar had become incredibly high. The reaction is another example of the market punishing “good but not great enough” results.

PVH fell 20% after particularly rough feedback. Very few investors had expected an outright revenue guidance cut, which has been rare this season. There is also concern that 1Q EPS and full-year EPS include a tariff refund benefit, meaning the underlying core result may represent a genuine miss and cut. This matters more broadly for Consumer because it connects directly to the new tariff headlines. If investors begin to question whether earnings are being supported by one-time tariff-related benefits, or whether new tariff pressure could hurt future margins, consumer discretionary and apparel could remain under pressure.

Derivatives reinforced the theme that index-level calm is masking major dispersion. As indices closed lower, the main vol story remained the push lower in implied and realized correlation. S&P implied correlation made new all-time lows, especially at the front end of the curve. This is a critical point. The market is not pricing or realizing a simple macro shock where all stocks move together. Instead, single-name and thematic dispersion remains extreme, while the index is being stabilized by offsetting winners and losers. That is why the Nasdaq can hold up even as rates, oil, and vol rise, and why sector/thematic tilts matter more than headline index direction.

The relative vol setup is also notable. Nasdaq vol is now 8 volatility points over S&P vol, making it difficult to realize that spread. The three-day average of the three-month implied vol ratio in QQQ versus SPY is at the highest level in seven years. The desk would rather own S&P volatility at an 8-vol discount and prefers selling Russell 2000 or Nasdaq volatility to fund it. In simple terms, S&P vol looks relatively cheap versus Nasdaq and Russell vol, particularly if macro risk increasingly shows up at the index level while single-name and thematic vol in Tech is already very expensive.

Index-option flows were muted, with attention concentrated in single names and megacap offerings. The straddle for the rest of the week closed at 78bps, covering jobless claims and NFP. With the S&P at 7,554, that implies roughly a 59-point move and a remaining week range of about 7,495 to 7,613. Given the JPM NFP framework, the market likely still wants a payrolls print in the 70k to 100k range with contained wage growth. But after today’s move in oil, rates, and tariffs, the tolerance for a hot wage or payroll print is probably lower. A hot number that pushes yields higher could hit crowded Tech and momentum, while a weak number could intensify concerns about the consumer at the same time input costs are rising.

The bottom line is that the rally is no longer being supported by clean macro relief. The market now has to contend with oil near $96, the 10-year yield at 4.90%, renewed Middle East escalation, proposed tariffs, and increasingly demanding earnings expectations. The fact that the Nasdaq held in relatively well shows that AI and megacap demand remain powerful, but the broader tape weakened, small caps sold off, and flows turned meaningfully negative. The key takeaway is to stay focused on dispersion: index moves may remain contained, but sector and thematic rotations are violent. In this setup, it makes sense to respect the still-resilient AI/megacap bid, but be more cautious on crowded names with elevated earnings bars, tariff-sensitive consumer/apparel, and areas vulnerable to higher oil and higher yields.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!