Institutional Insights: Credit Agricole "Risk Index - Investors Remain Confident'

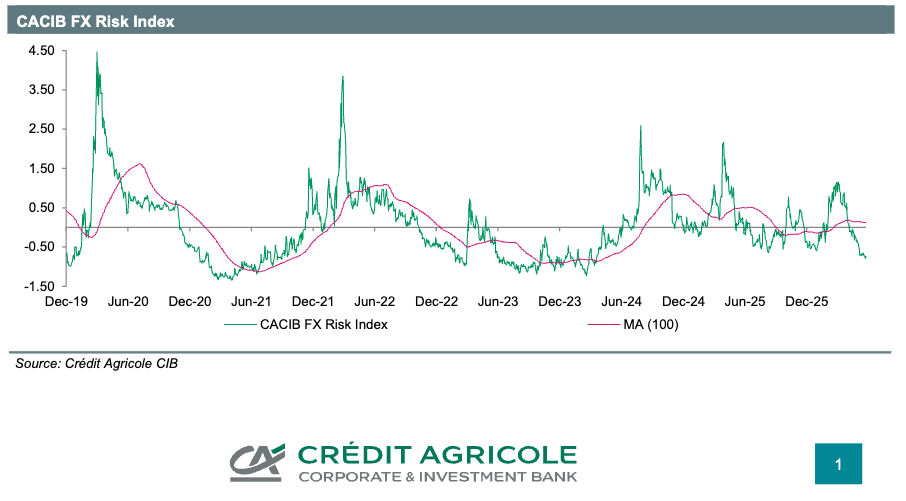

Investor confidence remains resilient despite the ongoing US-Iran impasse and continued exchange of fire. The Risk Index has fallen to -0.7343 from -0.7171 last week, reaching its lowest level in more than two years, and the trend in the index is now turning lower. In practical terms, that indicates a market still leaning risk-on rather than risk-off, with investors continuing to look through geopolitical volatility on the assumption that a deal will eventually be reached and that the closure of the Strait of Hormuz will ultimately end.

The key reason sentiment has held up is that investors still believe diplomacy will prevail, even though the two sides appear far apart. Markets are assigning weight to comments from US Secretary of State Marco Rubio that Iran’s Supreme Leader Ayatollah Mojtaba Khamenei is “increasingly engaging” in talks with the US, although there has been no confirmation from Iran that negotiations are ongoing. That lack of confirmation matters because the market’s confidence is being built on a fragile and headline-sensitive assumption: that back-channel or direct engagement is progressing despite public hostility.

The diplomatic hurdles remain meaningful. Iran has reportedly demanded a ceasefire in Lebanon between Hezbollah and Israel as a condition for continuing talks on extending the ceasefire. It is also demanding sanctions relief in exchange for re-opening the Strait of Hormuz. Rubio, however, has said sanctions relief would only come with an agreement on Iran’s nuclear programme. That leaves a substantial gap between the two sides. The market is not ignoring this gap, but it is discounting it for now because prior escalation has not yet translated into a durable broader shock to risk assets.

AI-related equities remain the other major support for sentiment. Even as oil, yields, and geopolitical headlines have moved against the market at times, the rally in AI infrastructure, semiconductors, megacap platforms, and selected software/security names has continued to provide an important offset. This is one reason index volatility has stayed relatively contained despite violent sector and factor rotation. The market can absorb geopolitical anxiety better when a powerful structural growth theme is still pulling capital into equities.

The next shift in focus is likely to be US macro data, especially the labor market. Sentiment will remain highly sensitive to whether higher oil prices are beginning to weigh on the US economy. A labor-market print suggesting that the economy is buckling under higher energy costs would likely hurt risk appetite, particularly because it would raise stagflation concerns rather than a clean soft-landing narrative. So far, however, the data indicate that the economy is holding up well. That is why investors remain willing to look through the Middle East conflict and maintain equity exposure.

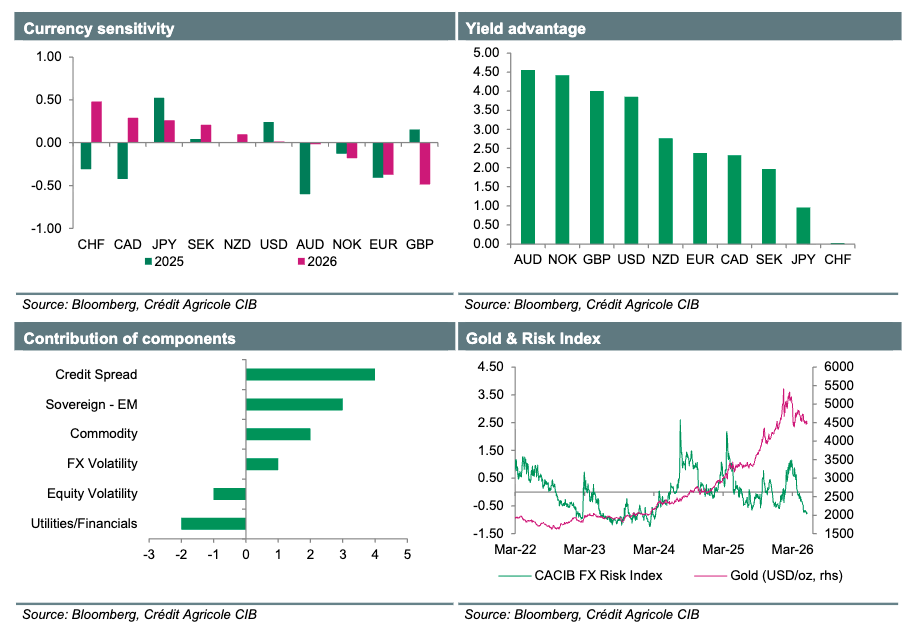

The components of the Risk Index show a mixed but still constructive backdrop. Falling equity-market volatility has weighed on the index, as has the outperformance of cyclical stocks over defensive stocks. Both are classic risk-on signals. At the same time, rising private credit spreads, wider emerging-market sovereign spreads, and higher gold prices have supported the index, reflecting that there is still caution in credit, sovereign risk, and safe-haven demand. This mix captures the current market well: equity investors remain confident, but cross-asset stress has not disappeared.

The FX correlations are also notable. Among G10 currencies, only the Swiss franc has a significant positive correlation with the Risk Index, meaning CHF tends to strengthen or behave more defensively when the index rises, consistent with its safe-haven role. The euro and sterling have significant negative correlations with the Risk Index, meaning they tend to perform better when risk conditions improve and the index falls. In the current environment, that implies continued risk confidence could be more supportive for EUR and GBP than CHF, while any geopolitical or credit shock that pushes the Risk Index higher would likely favor CHF.

The main takeaway is that investors are still treating Middle East escalation as a negotiable shock rather than a systemic one. The market remains confident that some form of US-Iran deal will eventually emerge, but that confidence is vulnerable because the political demands on both sides remain far apart. As long as oil does not create visible damage in US labor or consumer data, and as long as AI-linked equities remain bid, sentiment can stay resilient. But if labor data soften sharply, private credit spreads widen further, or diplomacy breaks down publicly, the current low-risk-index reading could reverse quickly.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!