Institutional Insights: Credit Agricole FX Weekly 12/6/26

Seven Holders, a New Chair, and a Comeback Win?

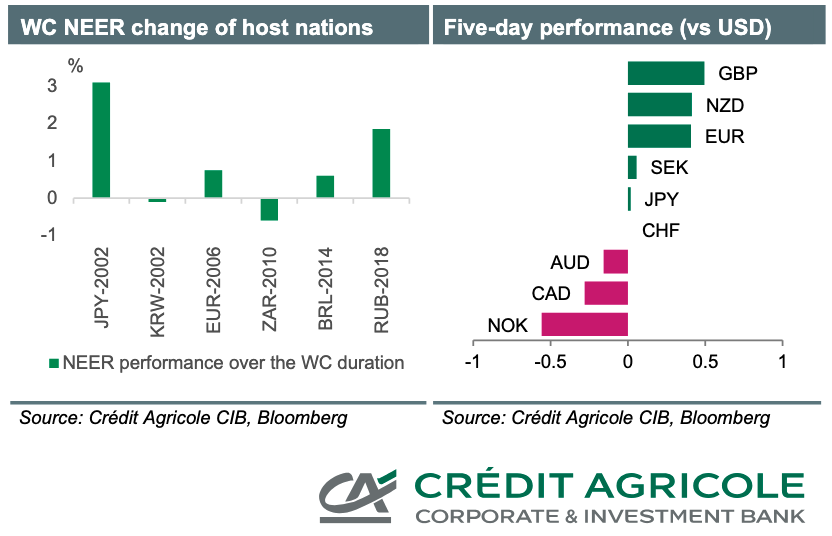

The title might not seem to fit FIFA's 2026 World Cup, which kicked off yesterday in Mexico. Historically, the tournament has had minimal impact on foreign exchange markets, often leading to muted price movements during the games. However, this week is packed with potential market movers, including a major G7 summit, seven central bank meetings, and a pivotal by-election in the UK.

The Federal Reserve is anticipated to maintain its current interest rates, but we could see a more hawkish tone in their statements and the Summary of Economic Projections (SEP). The upcoming June meeting will be particularly scrutinized as observers look to see how the newly appointed Fed Chair, Kevin Warsh, aligns his previously dovish outlook with the broader views of the Federal Open Market Committee (FOMC). Additionally, there may be updates on his proposed policy changes, such as reducing the balance sheet, discontinuing the dot plot, or adopting alternative measures for inflation. With many positive Fed expectations already factored into the market and a recent surge in long positions, the U.S. dollar may find it challenging to continue its upward trajectory.

On the other hand, downside risks for the British pound have increased recently, especially as we approach next week’s by-election and the Bank of England's policy meeting. A possible win for Andrew Burnham could shift FX investors' focus back to the looming political and fiscal uncertainties. Moreover, if the Bank of England continues to adopt a "wait and see" approach, it could lead to a reassessment of market rate expectations, undermining the pound’s relative rate advantage.

The Bank of Japan's upcoming decisions carry significant uncertainty. This isn’t just about Governor Kazuo Ueda potentially missing the meeting; it’s more about our economists predicting that any interest rate hike could come later than what JPY money markets have currently priced in. Even if a hike occurs, it would need to be notably hawkish to support the yen. The USD/JPY has established a solid base above 160, which could challenge the crucial 162-164 range—beyond which we might see a reversal of its post-Plaza Accord depreciation.

In other news, low inflation gives the Swiss National Bank (SNB) a strong rationale to maintain its loose monetary policy. Meanwhile, Sweden’s tax-related shortfall may provide the Riksbank with additional time before making moves, as they closely monitor rate hikes from the European Central Bank (ECB). Additionally, the two G10 central banks that raised rates earlier this year—the Reserve Bank of Australia (RBA) and Norges Bank—might consider pausing in June. This doesn’t undermine their potential for further tightening down the line, while both the Australian dollar and Norwegian krone could continue to benefit from their attractive carry appeal.

FX & Gold Outlook: King Dollar, Fragile Europe, Supported Gold

🌍 Big Picture

The core FX theme remains USD exceptionalism versus fragile non-US fundamentals.

The dollar should stay supported by:

- resilient US growth,

- sticky inflation,

- high carry,

- expensive USD hedging costs,

- reserve-currency dominance,

- continued portfolio and FDI inflows.

By contrast, Europe remains exposed to:

- geopolitical risk,

- weak growth,

- weaker competitiveness,

- tariff pressure,

- deteriorating net exports,

- domestic-demand-led fiscal stimulus that may not directly support EUR demand.

Gold remains structurally supported by concerns over fiscal sustainability, sticky inflation, and debt absorption risks across major economies.

🇺🇸 USD: Still the King of FX

The high-yielding safe-haven dollar should remain well supported, even if Middle East geopolitical risks begin to fade.

The US economy is still expected to outperform many European and Asian peers. That resilient growth backdrop, combined with sticky inflation, should continue to challenge the market’s still-dovish Fed pricing.

Policy uncertainty may persist, but the broader US exceptionalism narrative remains intact.

Key USD supports include:

- US growth outperformance,

- sticky inflation limiting Fed cuts,

- high carry,

- expensive hedging costs,

- potential unhedged portfolio inflows,

- expected FDI inflows,

- Fed institutional independence,

- limited risk of a coordinated “Mar-a-Lago accord” to weaken the dollar,

- lack of credible reserve-currency alternatives.

A bear-flattening in the UST curve could keep USD hedging costs prohibitively high, encouraging more unhedged inflows into US assets.

View: USD remains the cleanest long in G10, though investors may wait for confirmation that foreign portfolio inflows are continuing before adding aggressively.

🇪🇺 EUR: Collateral Damage

The euro should continue to trade as collateral damage from global geopolitical risk.

We remain bearish on EUR/USD from current levels, though expected ECB hikes should limit downside risks to some extent over the coming months.

The longer-term EUR story remains difficult. The currency continues to suffer from:

- subdued growth prospects,

- weaker international competitiveness,

- US tariff pressure,

- domestic-demand-driven Eurozone policy,

- weaker net exports,

- lower corporate demand for EUR-denominated assets.

German fiscal stimulus and other domestic-demand-led policies may support activity at the margin, but they are unlikely to improve the Eurozone’s external position. Instead, they could reduce net exports and weaken structural demand for EUR.

Many positives already appear priced into EUR/USD, as suggested by long-term fair value models.

View: EUR/USD remains a sell on rallies; ECB hikes can slow, but not reverse, the bearish trend.

🇨🇭 CHF: Safe-Haven Strength Meets SNB Resistance

The franc has reached new decade highs against both the EUR and USD, driven by persistent safe-haven demand.

The SNB has stepped up its defence against excessive CHF strength. In particular, EUR/CHF around 0.90 now looks like a line in the sand that the market is willing to respect.

For CHF to give back more ground, markets would likely need:

- reduced geopolitical risk,

- broader risk recovery,

- less demand for safe-haven assets,

- stronger confidence in European growth.

Until then, CHF should remain well supported, but further appreciation may be increasingly resisted by the SNB.

View: CHF remains strong, but EUR/CHF 0.90 is an important policy-sensitive floor.

🇯🇵 JPY: Takaichi Policy Mix Keeps Yen Under Pressure

We remain cautious on the yen.

Prime Minister Sanae Takaichi’s policy agenda should weigh on JPY through two channels:

1. holding back BoJ rate hikes,

2. higher fiscal spending that supports the Nikkei and risk appetite.

Higher oil prices from the Middle East conflict add another headwind by worsening Japan’s terms of trade.

The likely comfort zone for the BoJ and government appears to be USD/JPY 150–160. This range keeps the yen weak enough to support exports and corporate profits, while not adding excessive inflation pressure or drawing too much criticism from President Trump.

However, moves above 160 would increase the risk of:

- FX intervention,

- a faster BoJ hiking cycle,

- stronger political pressure to address imported inflation.

Inflation remains a key voter concern in Japan, so the government cannot ignore a weak-yen-driven inflation shock.

View: JPY remains under pressure, but USD/JPY above 160 becomes politically and policy-sensitive.

🇬🇧 GBP: UK Pressure Valve

We maintain a cautious outlook on GBP/USD, consistent with a bullish USD view.

Sterling could remain a key pressure valve for investors worried about potential UK political and fiscal instability. Persistent stagflation risks may fuel concerns over the UK’s economic and fiscal outlook.

The BoE may have limited ability to support the economy or ease the government’s fiscal burden, especially if inflation remains sticky.

That said, some bad news is already priced into GBP, particularly versus EUR. The Eurozone would also face major downside risks from a negative oil supply shock. GBP also looks oversold, while global investors appear underinvested in UK assets.

View: GBP/USD risks remain skewed lower, but EUR/GBP upside may be more limited given existing GBP pessimism.

🇨🇦 CAD: Range Holds, But Upside Risks to USD/CAD

USD/CAD has remained well anchored within 1.35–1.40 for most of the past year.

The CAD has weathered the dollar resurgence relatively well, helped by Canada’s positive terms-of-trade shock from higher energy prices.

However, the latest Fed repricing and resilient US macro data could tilt near-term risks toward the upside for USD/CAD.

View: CAD remains supported by energy, but strong USD momentum could push USD/CAD toward the upper end of the range.

🇦🇺 AUD: RBA Leadership Supports, But USD Caps Upside

The RBA’s rate-hike cycle is leading much of G10, helping AUD/USD maintain an upward trajectory in the first half of 2026.

Higher global energy prices are also somewhat insulating AUD from Middle East geopolitical stress through a positive terms-of-trade channel.

Still, the Fed’s reluctance to cut further and broad USD strength should limit AUD/USD upside. This could bring the pair modestly lower in the second half of 2026.

View: AUD supported in H1 by RBA and commodities, but USD strength caps gains into H2.

🇳🇿 NZD: Slow Grind Higher, But Oil Is a Risk

We expect a bounce in New Zealand’s economy and rising prospects of RBNZ hikes in the second half of 2026.

Supportive factors include:

- strong soft commodity prices,

- improving domestic momentum,

- reduced US equity outperformance relative to Asia,

- potential recovery in regional risk sentiment.

These should allow NZD/USD to grind gradually higher through 2026.

However, higher oil prices are a clear negative terms-of-trade shock for New Zealand. If the Middle East conflict persists, downside risks to NZD forecasts would increase.

View: NZD can recover slowly, but sustained high oil prices remain a key headwind.

🇳🇴 NOK: Energy Tailwind, But Rally May Pause

The NOK has been one of the best-performing G10 currencies this year.

It has benefited from:

- a more hawkish Norges Bank,

- higher energy prices,

- attractive valuation,

- improved carry appeal.

Year-to-date gains have already exceeded a bullish NOK call, so a near-term pause or consolidation looks likely.

That said, the NOK remains long-term undervalued, and more appreciation may be needed over time to correct that mispricing.

View: NOK may pause near term, but the medium-term valuation story remains constructive.

🇸🇪 SEK: Needs Stronger Domestic Evidence

The SEK has struggled this year after outperforming in 2025.

Near-term risks remain negative because of a potentially wider policy gap between the Riksbank and the ECB. If the ECB tightens more convincingly while the Riksbank lags, SEK may remain on the back foot.

For SEK to reverse course later this year, markets will need clearer evidence that Sweden is outperforming the Eurozone on macro fundamentals.

View: SEK remains vulnerable near term; recovery needs stronger Swedish macro data.

🟡 Gold: Debt, Inflation, and Fiscal Dominance Keep XAU Supported

Gold should remain supported by growing market concern that high government borrowing and sticky inflation across G10 economies will make public debt harder to absorb.

The key gold-supportive themes are:

- rising government borrowing,

- sticky inflation,

- concerns about debt sustainability,

- fears of fiscal dominance over the Fed,

- pressure on US real yields,

- safe-haven demand.

Fiscal dominance fears could weigh further on real yields, adding another tailwind for XAU.

To materially dent gold strength in 2026, markets would likely need a renewed rebound in the US economic outlook alongside higher real US rates and yields.

View: Gold remains structurally supported; dips should attract demand unless US real yields rise meaningfully.

🧭 Trade Map

| 🇺🇸 USD | Bullish | US exceptionalism, high carry, sticky inflation |

| 🇪🇺 EUR/USD | Bearish | Weak growth, tariffs, competitiveness loss |

| 🇨🇭 CHF | Supported | Safe-haven demand, SNB resistance near EUR/CHF 0.90 |

| 🇯🇵 JPY | Bearish, but intervention risk | Takaichi policy, oil shock, USD/JPY 160 risk |

| 🇬🇧 GBP/USD | Cautious/Bearish | UK fiscal-political risks, stagflation |

| 🇨🇦 CAD | Rangebound | Energy support vs strong USD |

| 🇦🇺 AUD/USD | H1 supported, H2 softer | RBA hikes, commodities, USD cap |

| 🇳🇿 NZD/USD | Gradual recovery | RBNZ hike risk, commodities, oil drag |

| 🇳🇴 NOK | Constructive medium term | Energy, Norges Bank, undervaluation |

| 🇸🇪 SEK | Near-term vulnerable | Riksbank/ECB policy gap |

| 🟡 Gold | Bullish | Debt fears, fiscal dominance, real-yield pressure |

The 2026 FX market remains a contest between USD exceptionalism and non-US fragility.

- Stay long USD selectively.

- Sell EUR/USD rallies.

- Treat JPY weakness as valid below USD/JPY 160, but be alert to intervention risk above it.

- Stay cautious on GBP/USD.

- Prefer NOK and selective commodity FX on valuation and carry.

- Keep gold exposure as a hedge against fiscal-dominance and debt-sustainability risks.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!