Daily Market Outlook, November 30, 2023

Daily Market Outlook, November 30, 2023

Munnelly’s Market Commentary…

Asia - .stocks concluded the month with a mixed and uncertain performance, despite notable gains, as uncertainty lingered around the Israel-Hamas truce, which was eventually extended for one more day. Investors grappled with significant data releases, including disappointing official PMI figures from China. The Nikkei 225 fluctuated between gains and losses, influenced by recent currency strength and mixed data, with better-than-expected Industrial Production offset by softer Retail Sales. The KOSPI managed to stay afloat following the Bank of Korea's decision to maintain unchanged rates while maintaining a restrictive policy stance until inflation converges to the target level. The Hang Seng and Shanghai Composite showed indecisiveness, facing slight pressure after Chinese PMI data revealed a slightly deeper contraction in factory activity, raising the possibility of further supportive measures. Additionally, the Biden administration is expected to announce tax credit rules aimed at limiting China's influence in the U.S. electric vehicle market. The complex array of factors contributed to the uncertainty in the regional markets.

Europe - The November Lloyds Business Barometer, released today, indicates a second consecutive monthly increase in business confidence, reaching its highest level since February 2022. Positive improvements were observed in both their own trading prospects and the outlook for the general economy. The services sector led the way, with sentiment reaching its highest point in over two years. Retail experienced a second consecutive monthly increase, and manufacturing reached a five-month high. Despite these positive trends, businesses faced intense inflationary pressures, with the net balance expecting to raise prices reaching a new high. Wage pressures also remained historically high, with little change from the previous month.Today's release of the Bank of England's Decision Maker Panel results is likely to be closely monitored by policymakers, with a focus on whether inflation expectations have decreased. It's important to note that these results were collected before the release of lower-than-expected October CPI data. Policymakers will also be keen to identify any indications of easing wage pressures.

In the Eurozone, the forecast for the flash CPI in November suggests further declines in both headline and core measures to 2.8% and 3.9%, respectively. If realised, this would mark the lowest level for headline inflation since July 2021 and core inflation since June 2022. Lower-than-expected German and Spanish inflation outcomes for November raise potential downside risks for today's Eurozone figures.

US - Stateside, attention is likely to focus on the weekly jobless claims data, given last week's unexpected decrease against the recent trend of increases. The key question is whether this is an anomaly or a sign that labor market pressures persist. October data for the Federal Reserve's preferred inflation measure, the PCE deflator, is also expected to align with the CPI release, showing declines in both the headline and core measures to 3.1% and 3.5%. The notable speakers on the agenda include Fed's Wiliams (who is a voter), ECB President Lagarde (once again), and BoE's Greene.

FX Positioning & Sentiment

Credit Agricole's FX month-end rebalancing model suggests a preference for buying the EUR against a basket of USD and GBP. According to the model: Month-end portfolio rebalancing flows are likely to involve USD selling across the board, with the strongest sell signal against the CAD. The corporate flow model further indicates EUR buying at the end of the month.

Based on these signals, Credit Agricole has entered a trade to buy the EUR against both the USD and GBP. The intention is to hold this position until 30 November at 17:00 GMT, unless the trade is stopped out with a loss limited to 1%..

CFTC Data

The release of CFTC data for the period of November 15-21, though delayed due to the holidays, offers insights into the evolving market sentiment. Despite the potential outdated nature of the data, it sheds light on the short-term trends leading up to the end of 2023. In November, the USD index witnessed a gradual decline, reflecting a more pessimistic Federal Reserve rate outlook. During the specified period, the EUR exhibited a 0.32% increase, suggesting a substantial addition to long positions in the EUR. Conversely, the JPY decreased by 1.32% as the U.S.-Japan spreads narrowed, indicating a likely reduction in significant short positions in the JPY. The GBP saw a 0.32% increase, attributed to less dovish language from the Bank of England and UK inflation staying above the target. Both the AUD and CAD experienced gains of 0.74% and 0.09%, respectively, driven by a positive outlook on China and a reduction in substantial short positions. Bitcoin (BTC) witnessed a 3.54% increase, accompanied by a reduction of 1,344 contracts as of November 14. Sellers were active leading up to a 2023 high, with 38k contracts being sold. While the data may be dated, it provides valuable clues about the short-term market direction during this period.

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0895-1.0900 (567M), 1.0925-35 (1.4BLN), 1.0950-55 (817M)

1.0965-75 (1.5BLN), 1.1000 (789M), 1.1015 (350M), 1.1030 (1BLN)

EUR/CHF: 0.9540 (470M), 0.9580 (480M), 0.9600 (250M)

GBP/USD: 1.2620 (300M), 1.2700 (725M)

EUR/GBP: 0.8670-75 (437M), 0.8700 (661M)

AUD/USD: 0.6580 (591M), 0.6600 (831M), 0.6650 (410M), 0.6665 (301M)

NZD/USD: 0.6100 (379M), 0.6200 (322M)

USD/CAD: 1.3495-1.3515 (1BLN), 1.3650 (303M)

USD/JPY: 145.95-146.10 (887M), 146.80 (500M),147.30-35 (600M)

147.70 (1.2BLN), 148.00-10 (1.1BLN), 148.30 (1.8BLN)

Overnight Newswire Updates of Note

China’s Factory Activity Shrinks Again In Sign Of Recovery Woes

China Investment Bank Bans Bearish Research, Displays Of Wealth

Bank Of Korea Holds Policy, Extending Inflation Fight Into 2024

Japan Output Rises More Than Expected As Yen Boosts Activity

Japan Retail Sales Climb 4.2% On Year In October

BoJ's Nakamura: Need More Time Before Tweaking Ultra-Easy Policy

Australia’s Capex Misses Estimates Even As Firms Bolster Plans

Andrew Bailey: I’m No Pessimist But UK Outlook Is Worst I’ve Seen

ONS ‘Experimental’ Data Lowers UK Unemployment Rate To 3.5%

British Companies Most Confident Since February 2022 - Lloyds

Israel And Hamas Extend Their War Truce For Another Day

Dollar Drifts Near Three-Month Low, Focus On Inflation Data

JPMorgan Sees Treasury Buybacks Lifting Auction Sizes In May

Oil Holds Two-Day Advance Ahead Of High-Stakes OPEC+ Meeting

OPEC+ Will Likely Reach Deal With Holdouts Before Meeting: RBC

Asia Stocks Closing In On Strongest Month Since January

Salesforce Jumps As Cost-Cutting Moves Propel Profit Outlook

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

SP500 Bias: Bullish Above Bearish Below 4540

Below 4519 opens 4485

Primary support 4420

Primary objective is 4600

20 Day VWAP bullish, 5 Day VWAP bullish

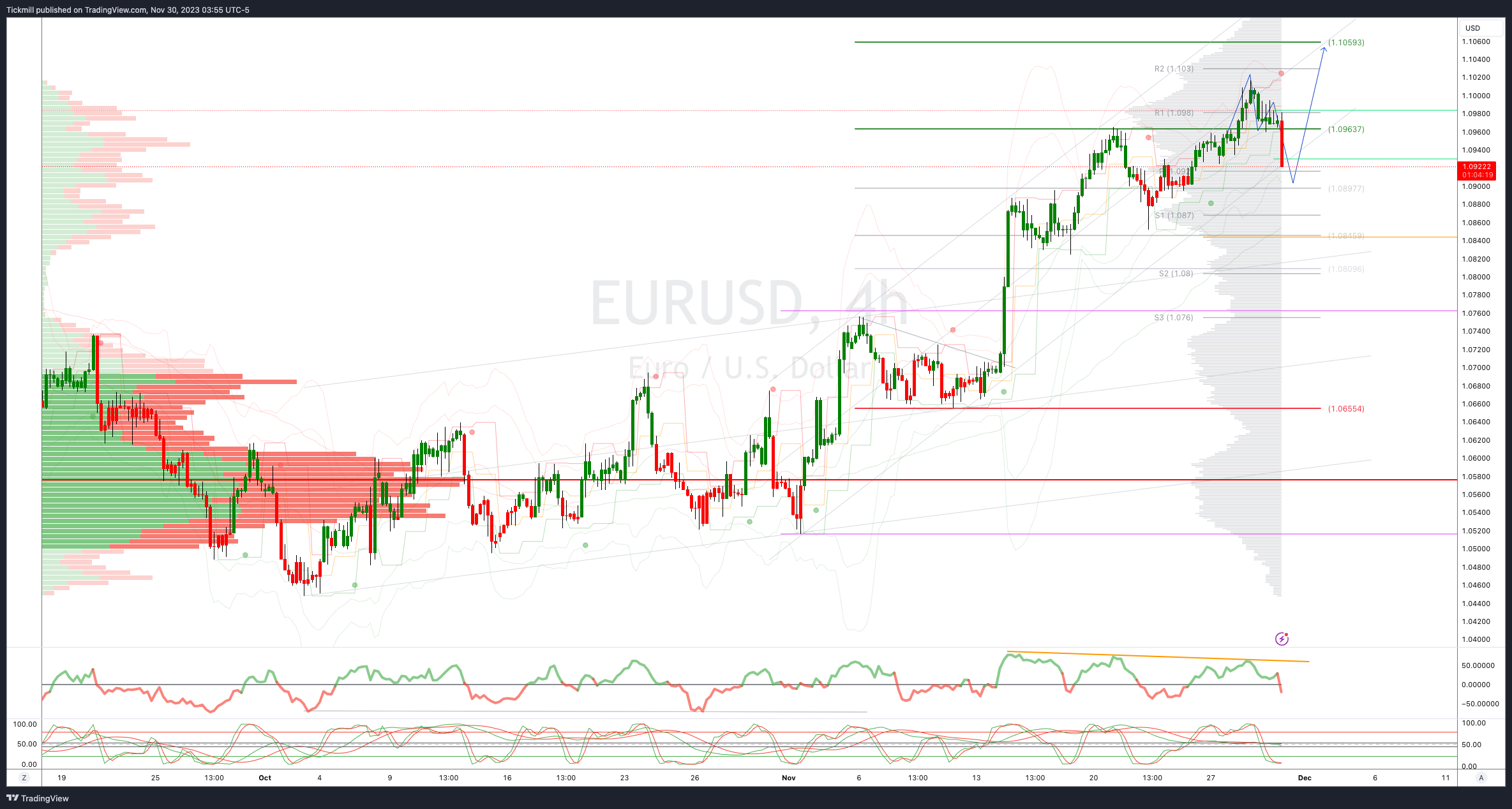

EURUSD Bias: Bullish Above Bearish Below 1.0950

Below 1.0940 opens 1.09

Primary support 1.0650

Primary objective is 1.1050

20 Day VWAP bullish, 5 Day VWAP bullish

GBPUSD Bias: Bullish Above Bearish Below 1.2640

Below 1.2630 opens 1.2575

Primary support is 1.2185

Primary objective 1.28

20 Day VWAP bullish , 5 Day VWAP bullish

USDJPY Bias: Bullish Above Bearish Below 148

Above 148.10 opens 149

Primary resistance 149.70

Primary objective is 145

20 Day VWAP bearish, 5 Day VWAP bearish

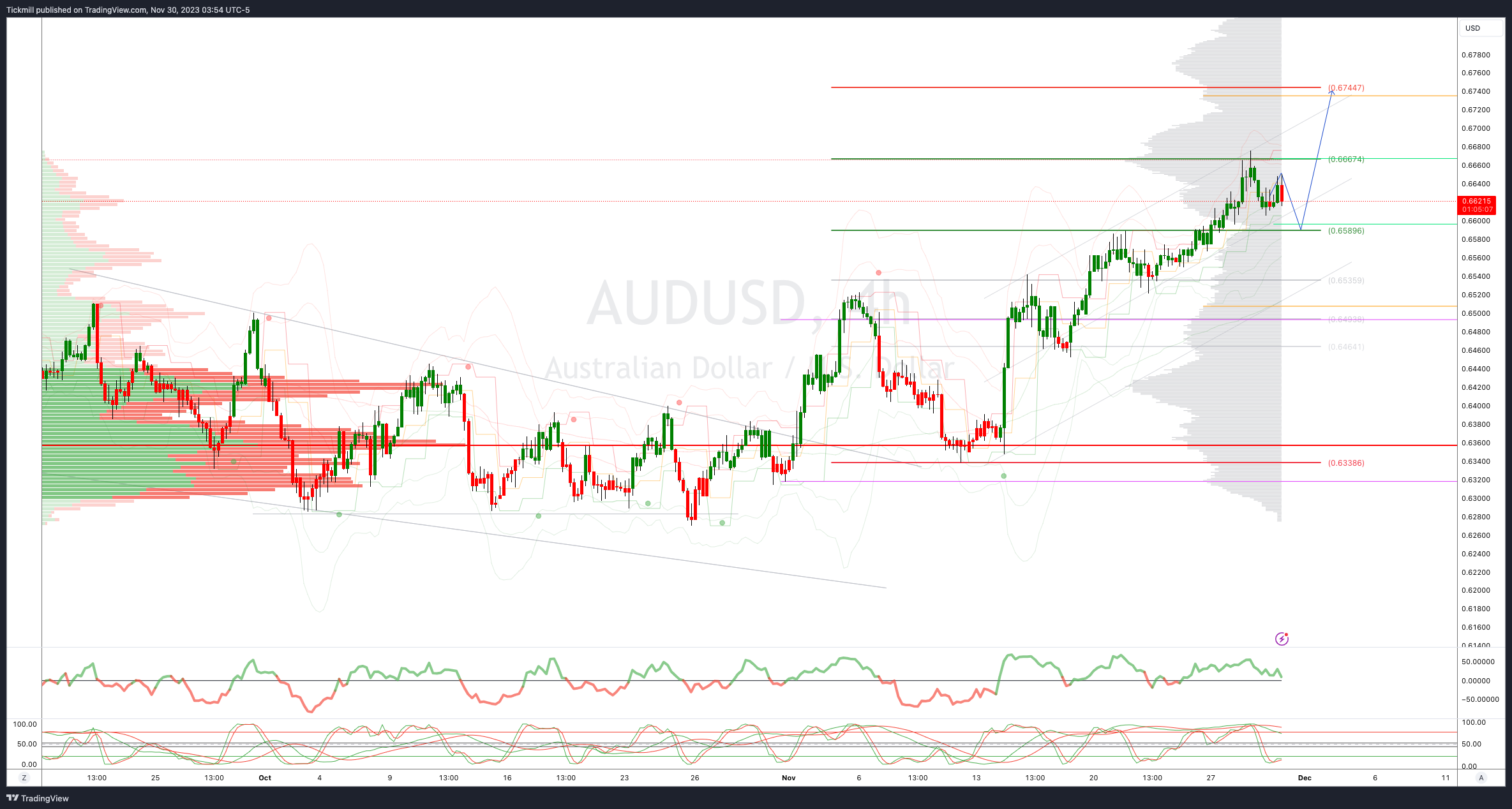

AUDUSD Bias: Bullish Above Bearish Below .6590

Below .6580 opens .6520

Primary support .6330

Primary objective is .6740

20 Day VWAP bullish, 5 Day VWAP bullish

BTCUSD Bias: Bullish Above Bearish below 34000

Below 33600 opens 32400

Primary support is 30000

Primary objective is 37000

20 Day VWAP bullish, 5 Day VWAP bullish

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!