Daily Market Outlook, November 28, 2023

Daily Market Outlook, November 28, 2023

Munnelly’s Market Commentary…

Asia - As the corporate month concludes, stocks in the Asia-Pacific region displayed a mixed performance, influenced by a lower yield environment and the lacklustre performance of US stocks. The Nikkei 225 index struggled to maintain early gains, facing profit-taking amid a strengthening currency. The Hang Seng index and Shanghai Composite index also recorded modest losses, despite support pledges from the PBoC, following a report indicating potential significant losses and job cuts in China's property sector, impacting banks.

Europe - This week in the UK, attention remains on the Autumn Statement, which has received positive feedback from business organisations. The focus extends to speeches by several Bank of England ratesetters, providing insights into their initial views on whether the announced fiscal measures might impact the inflation outlook. Today, external MPC member Jonathan Haskel is scheduled to discuss inflation. Additionally, the House of Commons Treasury Select Committee is set to question the Office for Budget Responsibility today, preceding Chancellor Jeremy Hunt's appearance on Wednesday. This sequence of events adds to the ongoing discussions surrounding fiscal policies and their potential implications on various economic aspects, particularly inflation.

In today's lineup of ECB speakers, German central bank head Nagel expresses openness to higher interest rates, suggesting a willingness to consider adjustments. Chief Economist Lane, on the other hand, appears to align more closely with the consensus middle ground, likely favouring the maintenance of interest rates at their current levels in the foreseeable future. Additionally, ECB President Lagarde is scheduled to deliver pre-recorded remarks, adding further insights into the central bank's perspective. On the economic data front, today's focus includes Eurozone M3 money supply growth, with expectations pointing towards a continued negative year-on-year basis. This data will contribute to the broader assessment of economic conditions in the Eurozone.

US - Stateside, The upcoming speech on the economic outlook by the Fed's Waller is expected to be a significant focus for markets. Although it is highly unlikely for the Fed to make changes to interest rates at its final policy meeting of the year next month, investors will be closely watching for any indications of how strongly policymakers might resist expectations for lower interest rates in 2024. Additionally, the opening remarks by the dovish Fed member Goolsbee at a separate event will be carefully monitored for insights into the central bank's policy sentiments.

In addition to these speeches, the Conference Board is set to release US consumer confidence data. Forecasts suggest a potential fourth consecutive monthly decrease in November, pointing towards a possible slowdown in consumer spending after strong growth in Q3. This release will offer valuable insights into the sentiments and expectations of US consumers, shaping the broader economic outlook.

FX Positioning & Sentiment

This week, the markets will be influenced by FX hedge rebalancing flows at the end of the month. According to models from Citibank and Barclays, the preliminary estimates indicate a stronger than average sell signal for the USD in November. For those investors who have proportional asset allocated portfolios, CitiQuant's model predicts outflows from global equities and inflows into global bonds, with the strongest inflows going into Canadian and Asian bonds. The FX hedging model suggests that the USD selling may stand out against both the AUD and NZD. The AUD/USD and NZD/USD are currently testing their respective 200 daily moving averages, and a close above those levels would be a bullish sign for the antipodeans. Additionally, the NZD/USD will face the Reserve Bank of New Zealand on Wednesday and is currently being drawn to large 0.6100 FX option expiries. The USD is on track to have its weakest monthly performance in a year and is unlikely to do any better in December, which is typically its worst month for performance.

CFTC Data

The release of CFTC data for the period of November 15-21, though delayed due to the holidays, offers insights into the evolving market sentiment. Despite the potential outdated nature of the data, it sheds light on the short-term trends leading up to the end of 2023. In November, the USD index witnessed a gradual decline, reflecting a more pessimistic Federal Reserve rate outlook. During the specified period, the EUR exhibited a 0.32% increase, suggesting a substantial addition to long positions in the EUR. Conversely, the JPY decreased by 1.32% as the U.S.-Japan spreads narrowed, indicating a likely reduction in significant short positions in the JPY. The GBP saw a 0.32% increase, attributed to less dovish language from the Bank of England and UK inflation staying above the target. Both the AUD and CAD experienced gains of 0.74% and 0.09%, respectively, driven by a positive outlook on China and a reduction in substantial short positions. Bitcoin (BTC) witnessed a 3.54% increase, accompanied by a reduction of 1,344 contracts as of November 14. Sellers were active leading up to a 2023 high, with 38k contracts being sold. While the data may be dated, it provides valuable clues about the short-term market direction during this period.

FX Options Expiries For 10am New York Cut

(1BLN+ represent larger expiries, more magnetic when trading within daily ATR)

EUR/USD: 1.0835-55 (2.3BLN), 1.0880 (457M), 1.0900 (818M)

1.0930 (411M), 1.0960-65 (300M), 1.1000 (837M)

USD/CHF: 0.8915 (644M). GBP/USD: 1.2650 (243M)

EUR/GBP: 0.8670 (211M), 0.8700-10 (897M), 0.8730 (397M)

AUD/USD: 0.6570-85 (1.1BLN), 0.6600 (388M)

NZD/USD: 0.6045-50 (642M), 0.6100 (670M). AUD/NZD: 1.0910 (401M)

USD/JPY: 147.50 (413M), 147.85-90 (820M), 148.50 (1.5BLN), 149.00 (1.8BLN)

149.25-30 (725M), 149.40-50 (1BLN)

Overnight Newswire Updates of Note

RBA Gov Bullock: Australia Inflation Path Similar To Overseas

Australia Retail Sales Unexpectedly Fall As Rate Hikes Take Toll

BoE Dep Gov Ramsden: Policy Needs To Be Restrictive For Sufficiently Long

UK Shop Price Inflation Slows To Lowest Rate In Over A Year

ECB's De Cos: It's Too Premature To Talk About Rate Cuts

Japan To Give Tax Breaks To Domestic EV, Chip Production - Nikkei

Hedge Fund Dollar Bulls Hold Fast Even As US Currency Erases Gains

BofA Sees Dollar Weakness, Aussie Rebound In ’24 As Fed Cuts

Traders Reload On Big Fed Rate Cut Bets, Target Multiple Easing

Saudi Arabia Seeks OPEC+ Oil Quota Cuts While Some Members Resist

Hedge Funds Slashed Bullish Oil Wagers Ahead Of OPEC+ Meeting

HSBC Sees ‘Very Low’ Chance Of OPEC+ Opting For Deeper Oil Curbs

Wall Street's 5,000 Club Grows On S&P 500 Optimism

Volkswagen Executives Warn Works Council Of Job Cuts

Barclays Explores Plan To Drop Thousands Of Investment Banking Clients

(Sourced from Bloomberg, Reuters and other reliable financial news outlets)

Technical & Trade Views

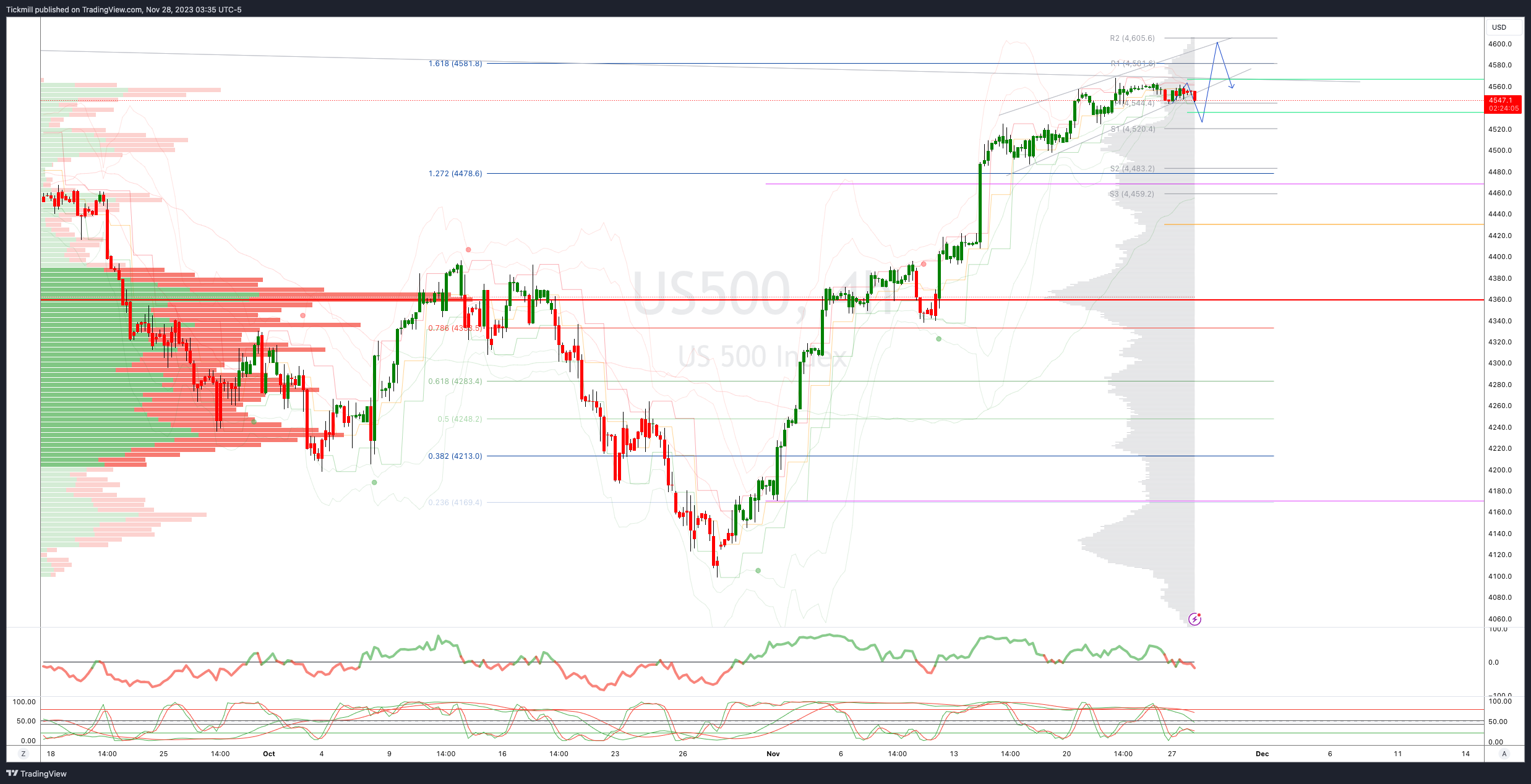

SP500 Bias: Bullish Above Bearish Below 4540

Below 4519 opens 4485

Primary support 4420

Primary objective is 4600

20 Day VWAP bullish, 5 Day VWAP bearish

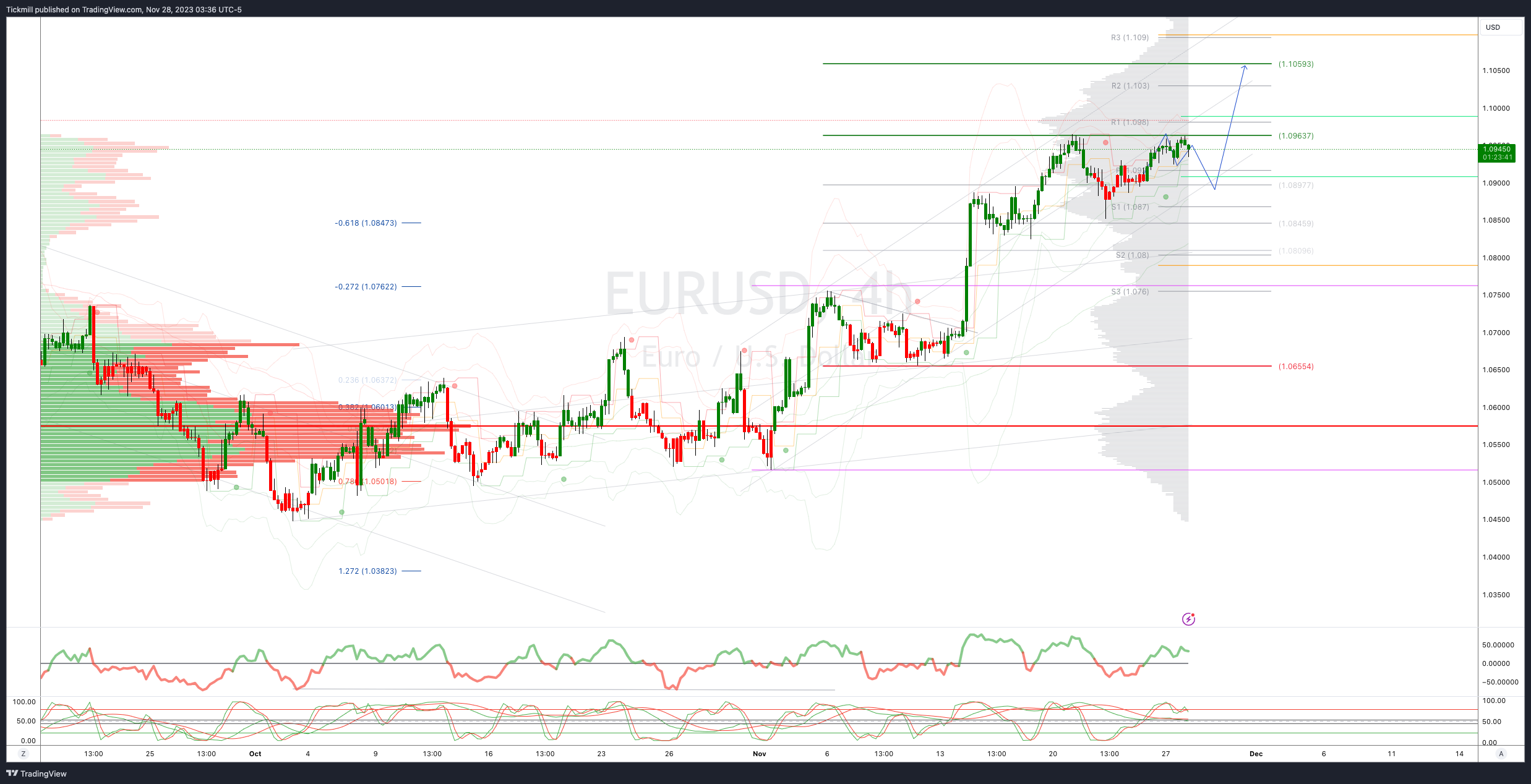

EURUSD Bias: Bullish Above Bearish Below 1.09

Below 1.08 opens 1.0750

Primary support 1.0650

Primary objective is 1.10

20 Day VWAP bullish, 5 Day VWAP bullish

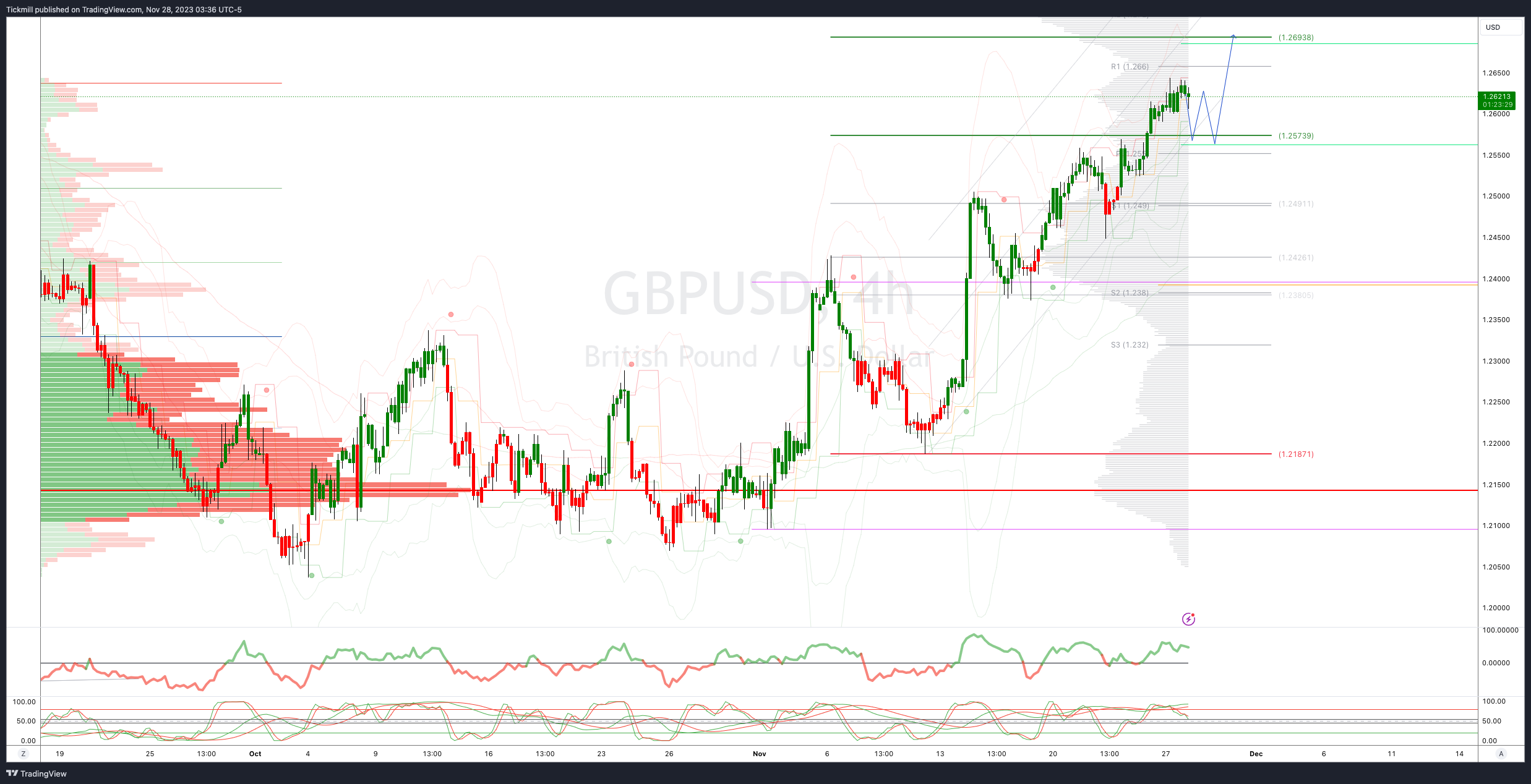

GBPUSD Bias: Bullish Above Bearish Below 1.2550

Below 1.24 opens 1.2350

Primary support is 1.2185

Primary objective 1.2690

20 Day VWAP bearish, 5 Day VWAP bullish

USDJPY Bias: Bullish Above Bearish Below 149

Above 149 opens 149.80

Primary resistance 147.30

Primary objective is 147

20 Day VWAP bearish, 5 Day VWAP bearish

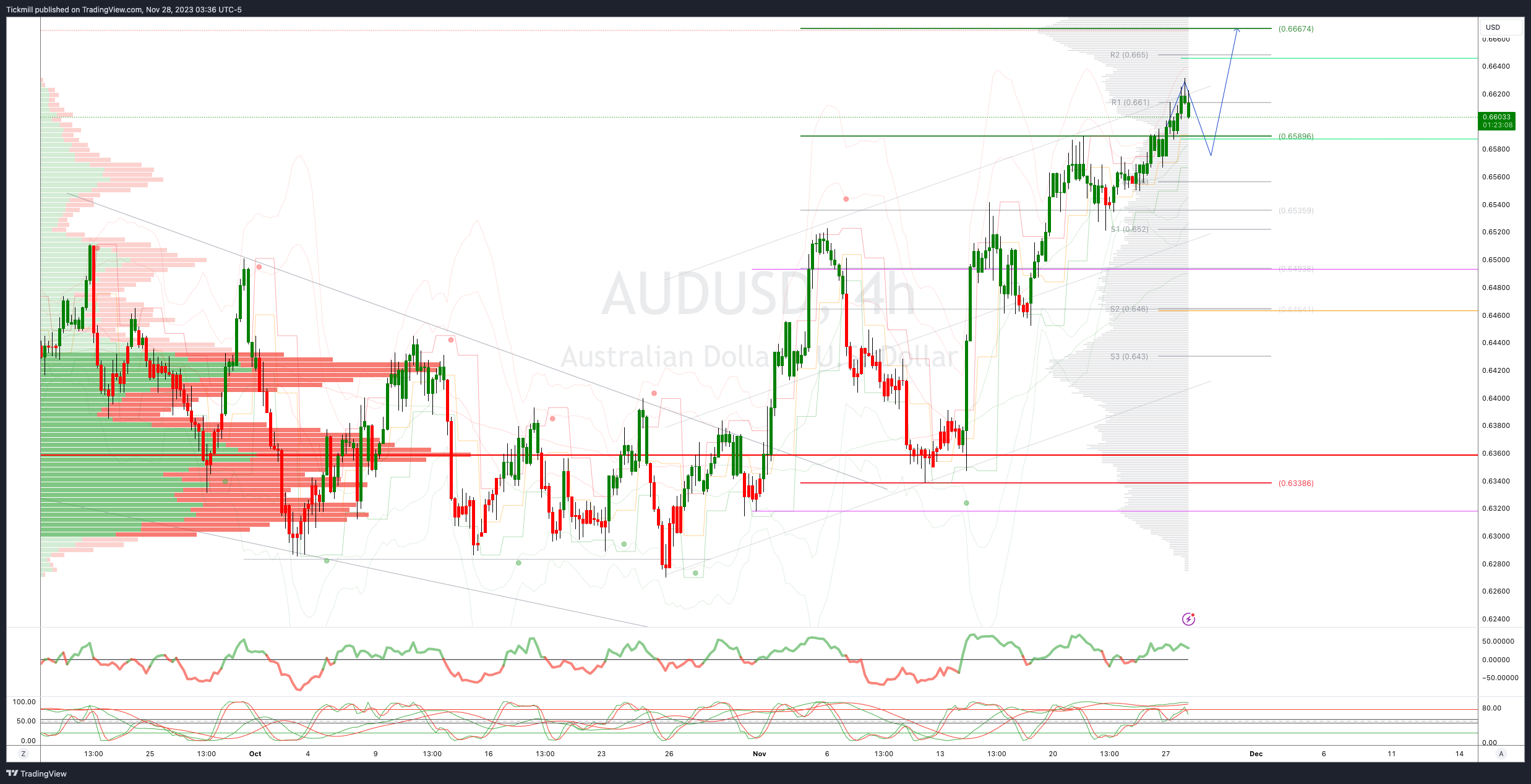

AUDUSD Bias: Bullish Above Bearish Below .6590

Below .6500 opens .6420

Primary support .6330

Primary objective is .6667

20 Day VWAP bullish, 5 Day VWAP bullish

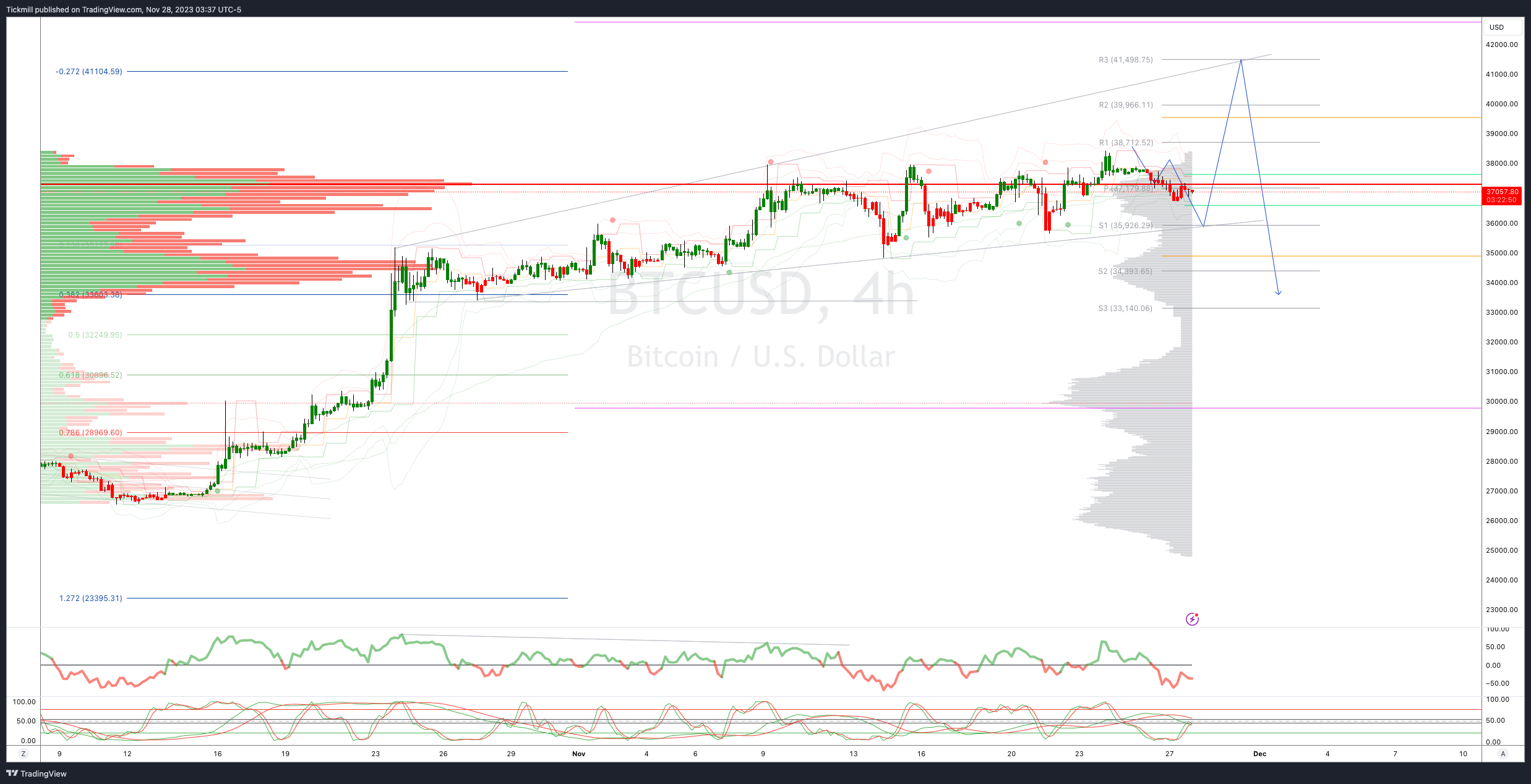

BTCUSD Bias: Bullish Above Bearish below 34000

Below 33600 opens 32400

Primary support is 30000

Primary objective is 37000

20 Day VWAP bullish, 5 Day VWAP bearish

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!